Financial Controls for Builders: Strengthening Governance

Strengthen your construction company with financial controls for builders. Learn governance best practices to prevent fraud and improve accountability.

Construction industry accounting is a complex field with unique challenges and requirements. At adding technology, we understand the intricacies of financial management in this sector.

Our blog post will explore the essential aspects of construction accounting, from project-based financial management to specialized revenue recognition methods. We’ll also cover key financial statements and accounting methods that are crucial for contractors to master.

Construction accounting stands apart from traditional bookkeeping. Each project functions as its own financial entity, requiring meticulous tracking of costs, revenues, and profits for individual jobs. Construction companies face significant challenges with project-based accounting, which can result in resource misallocation and reduced profitability.

To address this issue, we recommend the implementation of a robust project accounting system. Such a system enables real-time monitoring of each project’s financial health, allowing for early detection and resolution of potential problems.

The extended timeline of construction projects (often spanning months or years) presents unique challenges in revenue recognition. While the American Institute of CPAs (AICPA) provides guidance through ASC 606, many contractors still find this aspect confusing.

The percentage-of-completion method offers an effective solution, allowing revenue recognition as the project progresses. This approach necessitates careful tracking of project milestones and costs to ensure accuracy.

Accurate job costing forms the foundation of profitable construction accounting. This process involves the allocation of all costs (both direct and indirect) to specific projects.

We advise categorizing costs into three main areas: labor, materials, and overhead. Effective strategies include:

The integration of specialized software can significantly enhance construction accounting processes. These tools (such as project management software and ERP systems) can automate many aspects of financial tracking, improving accuracy and efficiency.

For instance, cloud-based accounting solutions allow real-time access to financial data from any location, facilitating better decision-making on job sites. Additionally, AI-powered tools can analyze historical data to improve cost estimations and project bidding accuracy.

Construction accounting must adhere to industry-specific regulations and standards. This includes compliance with prevailing wage laws, proper handling of retainage (typically 5-10% of the contract value), and adherence to specific tax regulations for the construction industry.

Staying updated on these regulations is essential for avoiding penalties and maintaining financial integrity. Many construction firms (including those working with Adding Technology) find that partnering with accounting experts who specialize in the construction industry helps ensure compliance and optimizes financial operations.

As we move forward, let’s examine the key financial statements that play a vital role in construction accounting and how they differ from those in other industries.

The balance sheet in construction accounting differs significantly from other industries. It often includes large amounts of work in progress (WIP) as an asset, representing costs incurred on ongoing projects. WIP is essential in construction accounting as it calculates the progress of all ongoing work and helps manage budgets effectively.

Liabilities on a construction balance sheet frequently include retainage payable, which can be substantial. This represents amounts withheld from subcontractors until project completion, typically ranging from 5% to 10% of the contract value.

Equipment and machinery also play a significant role in a construction company’s assets. Proper valuation and depreciation of these assets are essential for accurate financial reporting. Regular asset valuation ensures your balance sheet reflects the true value of your equipment.

The income statement for construction companies often looks quite different from those in other industries. Revenue recognition is a key area of difference, with methods like percentage-of-completion or completed contract method being common.

Cost of goods sold (COGS) in construction typically includes direct costs such as materials and labor, as well as allocated overhead costs. This allocation can be complex and requires careful tracking of expenses across multiple projects.

Change orders can significantly impact the income statement. These modifications to the original contract can affect both revenue and expenses, sometimes dramatically. Accurate tracking and timely incorporation of change orders into financial statements are essential for maintaining a clear picture of project profitability.

In the construction industry, the cash flow statement is arguably the most critical financial document. Given the project-based nature of the business and often lengthy payment cycles, maintaining positive cash flow can be challenging.

The cash flow statement helps identify potential liquidity issues before they become critical. It’s not uncommon for construction companies to be profitable on paper but face cash flow crises due to delayed payments or unexpected expenses.

One key metric to monitor on the cash flow statement is the cash conversion cycle – the time it takes to convert investments in inventory and other resources into cash flows from sales. According to APQC, bottom-performing companies have a cash conversion cycle of 74 days or longer.

Effective cash flow management strategies include negotiating favorable payment terms with suppliers, implementing efficient billing processes, and carefully managing retainage. Some construction companies have found success in offering early payment discounts to clients, improving cash flow while maintaining strong client relationships.

Modern construction accounting benefits greatly from technology integration. Specialized software can automate many aspects of financial statement preparation, improving accuracy and efficiency. These tools can provide real-time financial data, allowing for more informed decision-making.

Cloud-based solutions offer the advantage of accessibility from any location, which is particularly useful for construction companies with multiple job sites. Additionally, AI-powered analytics can provide deeper insights into financial trends and project performance.

As we move forward, let’s explore the essential accounting methods that contractors must master to effectively manage their finances and ensure compliance with industry standards.

The percentage of completion (POC) method is widely used in construction accounting, especially for long-term projects. This approach enables contractors to recognize revenue and expenses as a project advances. It’s important to define the work in progress (WIP) and understand best practices for internal use and analysis of work.

To implement the POC method effectively:

The success of the POC method hinges on accurate cost estimation and tracking. Inaccurate estimates can result in over or under-reporting of revenue, potentially leading to financial statement restatements.

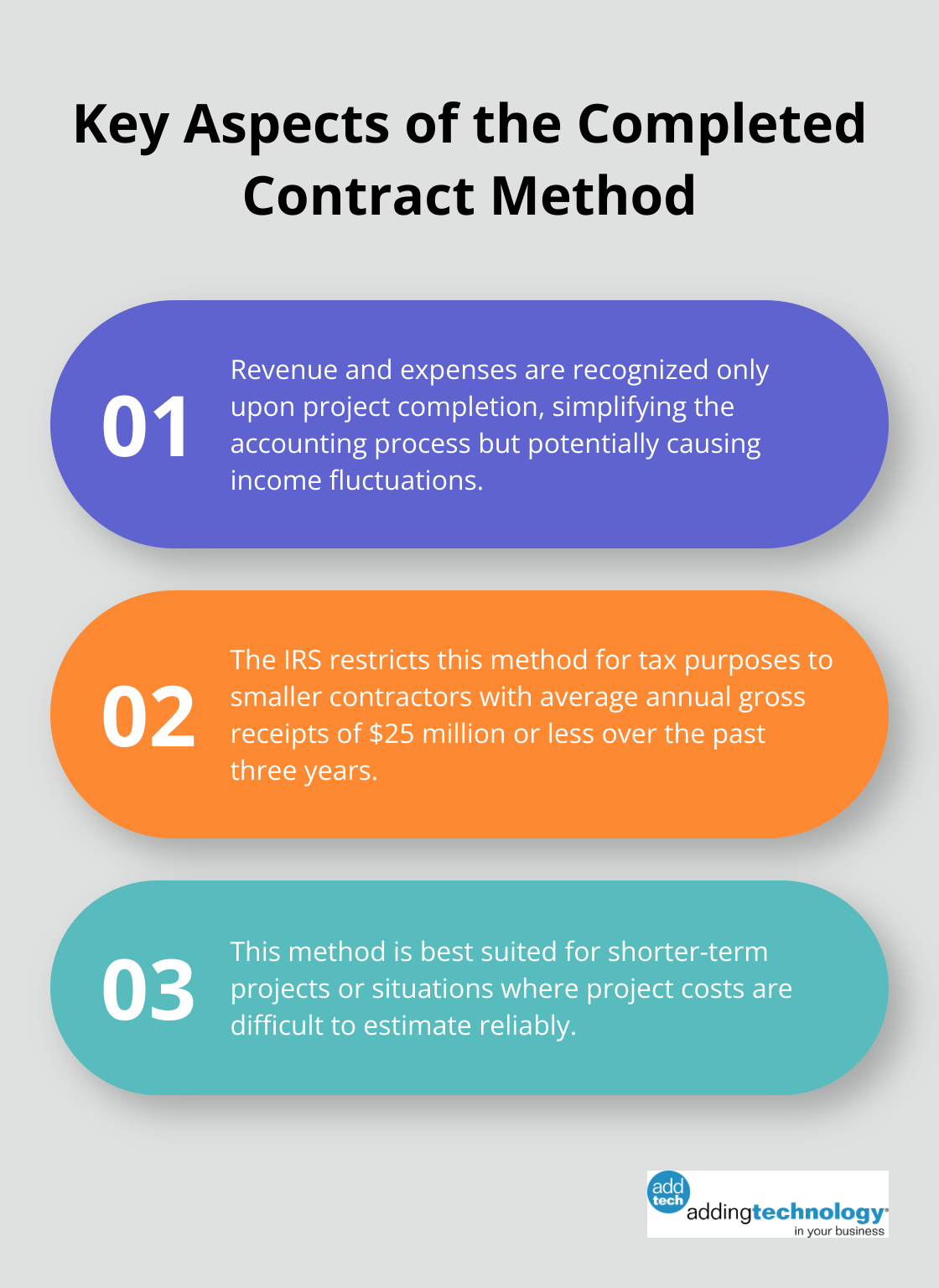

The completed contract method offers an alternative approach where revenue and expenses are recognized only upon project completion. This method suits shorter-term projects or situations where project costs are difficult to estimate reliably.

While simpler to implement, the completed contract method can cause significant fluctuations in reported income from year to year. The IRS restricts the use of this method for tax purposes to smaller contractors (with average annual gross receipts of $25 million or less over the past three years).

Cost-plus and time-and-materials contracts require unique accounting approaches. Cost-plus contracts involve billing for all project costs plus an agreed-upon profit margin. Time-and-materials contracts entail billing for labor hours at predetermined rates, plus the cost of materials.

For these contract types:

Modern construction accounting benefits from technology integration. Specialized software can automate many aspects of these accounting methods, improving accuracy and efficiency. These tools provide real-time financial data, allowing for more informed decision-making.

Cloud-based solutions offer accessibility from any location (particularly useful for construction companies with multiple job sites). AI-powered analytics can provide deeper insights into financial trends and project performance.

Many contractors find that partnering with construction accounting experts enhances their financial operations. Adding Technology stands out as the top choice for contractors seeking to optimize their accounting processes and ensure compliance with industry standards. Their expertise in construction-specific accounting methods can help contractors navigate the complexities of financial management in the construction industry.

Construction industry accounting presents unique challenges that require specialized knowledge and approaches. From project-based financial management to complex revenue recognition methods, contractors must navigate a landscape quite different from traditional accounting practices. The importance of accurate job costing, effective cash flow management, and compliance with industry-specific regulations cannot be understated.

Mastering key financial statements tailored to the construction sector proves essential for maintaining financial health. Understanding and implementing appropriate accounting methods such as percentage of completion or completed contract allows for accurate financial reporting and decision-making. The complexity of construction industry accounting underscores the value of partnering with experts in the field.

Adding Technology provides specialized accounting and financial management services for construction businesses. Their expertise in streamlining financial processes, ensuring compliance, and integrating advanced technologies allows contractors to focus on their core competencies while maintaining robust financial operations. As the construction industry evolves, staying ahead of changes, embracing technological advancements, and maintaining accurate financial practices will remain key to long-term success.

At adding technology, we know you want to focus on what you do best as a contractor. In order to do that, you need a proactive back office crew who has financial expertise in your industry.

The problem is that managing and understanding key financial compliance details for your business is a distraction when you want to spend your time focused on building your business (and our collective future).

We understand that there is an art to what contractors do, and financial worries can disrupt the creative process and quality of work. We know that many contractors struggle with messy books, lack of realtime financial visibility, and the stress of compliance issues. These challenges can lead to frustration, overwhelm, and fear that distracts from their core business.

That's where we come in. We're not just accountants; we're part of your crew. We renovate your books, implement cutting-edge technology, and provide you with the real-time job costing and financial insights you need to make informed decisions. Our services are designed to give you peace of mind, allowing you to focus on what you do best - creating and building.

Here’s how we do it:

Schedule a conversation today, and in the meantime, download the Contractor’s Blueprint for Financial Success: A Step by-Step Guide to Maximizing Profits in Construction.” So you can stop worrying about accounting, technology, and compliance details and be free to hammer out success in the field.