Financial Controls for Builders: Strengthening Governance

Strengthen your construction company with financial controls for builders. Learn governance best practices to prevent fraud and improve accountability.

Most construction business owners we work with at adding technology admit they don’t fully understand their financial statements. Yet these numbers are the difference between a thriving business and one that runs out of cash mid-project.

Financial statements for builders aren’t just accounting paperwork-they’re your business dashboard. This guide walks you through the three core statements, shows you how to spot problems early, and explains how to use your numbers to make smarter decisions about pricing, growth, and profitability.

Your income statement shows what you actually earned on each job and where your money went. Revenue gets recorded using the percentage-of-completion method, which ties what you recognize as income directly to how much work you’ve finished on a project. This matters because it gives you real-time visibility into whether a job is profitable before it’s done.

Direct costs like labor, materials, and subcontractors come off first to show gross profit on that specific project. Then overhead and indirect costs come out to show your net income. Many builders skip this step and only look at cash in the bank, which is why they get surprised when a profitable-looking project actually loses money once all costs are accounted for.

The balance sheet is a snapshot of what your company owns, owes, and what’s actually yours. Current assets include cash, accounts receivable from clients, and retainage that clients hold back. Fixed assets are your equipment, vehicles, and property.

On the liability side, you have short-term debts due within a year and long-term debt like equipment loans. The gap between assets and liabilities is your equity, which represents the real value of your business. A healthy balance sheet shows you have enough current assets to cover current liabilities, which signals you can fund operations and chase new work without constantly borrowing.

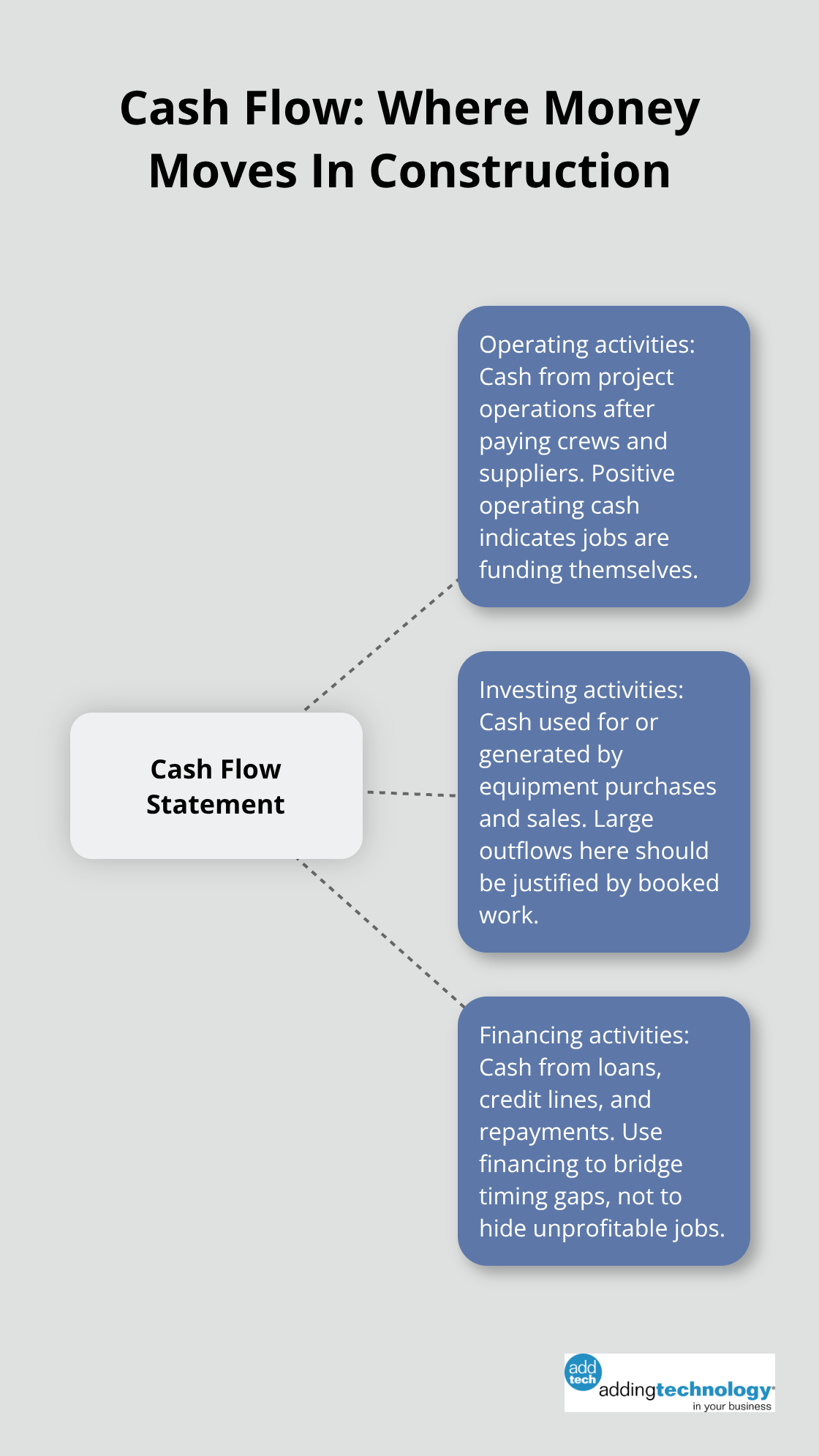

The cash flow statement is where most builders get blindsided. You can show profit on your income statement while having negative cash flow in reality. This happens because revenue gets recognized when work is done, but cash from clients arrives weeks or months later through progress payments.

Operating activities show whether your jobs actually generate cash after paying crews and suppliers. Investing activities track equipment purchases and sales. Financing activities show debt and credit movements. Research indicates that construction firms experience cash flow challenges throughout project cycles, with negative cash flow occurring for significant portions of project duration.

A practical approach is reviewing six months of historical data to see if completed projects consistently generated more cash than they spent on labor and materials. If they didn’t, your pricing is too low or your cost control is broken. Equipment investments should only happen if you have booked work to justify them, not just because you think you might need capacity later.

These three statements work together to paint a complete picture of your financial health. Your income statement tells you if jobs are profitable, your balance sheet shows whether you have the resources to operate, and your cash flow statement reveals whether you actually have money in the bank to pay your crew and suppliers. Understanding how they connect prepares you to spot problems before they become crises.

Gross profit margin tells you what percentage of revenue remains after direct costs like labor, materials, and subcontractors. If your gross profit margin drops below 25 percent on a job, that’s a warning sign your pricing is too low or your costs are running wild. Track this number job by job, not just across your entire operation, because one underpriced project can hide profitability problems on others.

Net profit margin goes deeper by including overhead and indirect costs, showing what you actually keep after everything gets paid. Most construction firms operate with net margins between 5 and 10 percent according to Construction Financial Management Association benchmarks, so if you’re below that range consistently, your business model has structural problems that won’t fix themselves.

Cash flow problems sneak up because they don’t show on your income statement. A job can look profitable while draining your bank account if your clients are slow to pay. Days in accounts receivable measures how long your money sits with clients before hitting your bank account.

If this number climbs above 45 days, your cash flow gets squeezed hard, and you need to tighten collections immediately or adjust your payment terms. Compare this metric month to month and watch for creeping increases that signal clients are paying slower. Rising values in this metric demand your attention before cash shortages force difficult decisions about payroll or supplier payments.

Cost overruns reveal themselves through two numbers you should review weekly on active jobs: actual labor hours versus estimated labor hours, and actual material costs versus budgeted material costs. If a framing phase is 60 percent complete but labor hours are already at 75 percent of budget, you will overrun that job. The same applies to materials.

Most construction accounting software now flags these variances automatically, so you catch problems while there’s still time to adjust staffing, schedule, or client communication rather than discovering the damage after the job closes. This early warning system transforms your financial data from a historical record into an active management tool that protects your margins before they disappear.

Your financial statements only matter if they change how you bid, price, and grow. Most builders collect this data monthly and then ignore it until tax season, which means they leave money on the table on every single project. This pattern separates contractors who build sustainable businesses from those who bounce from crisis to crisis.

Start with a job that finished in the last quarter and compare actual performance against your estimates for labor hours, material costs, and timeline against what actually happened. If framing took 240 hours but you bid 200, that 20 percent overrun tells you something critical about either your estimating process or your crew efficiency. Pull your last ten completed jobs and you’ll spot patterns that your financial statements alone never reveal.

If labor consistently runs 15 to 20 percent over estimate, your pricing is fundamentally broken because you’re bidding on assumptions that don’t match reality. This isn’t a one-time problem to fix on a single job-it’s a systemic issue in how you estimate. Adjust your labor rates upward across the board or your net margins will continue shrinking.

If material costs run over, investigate whether you’re experiencing waste on site, whether suppliers are charging you more than you budgeted, or whether scope creep adds materials that weren’t priced. Each source requires a different fix, and your financial data points you toward the right answer.

Equipment investments should follow directly from this analysis. If your jobs consistently show you need a second crew or specialized equipment to stay on schedule, that equipment purchase gets justified by real project data, not speculation. A $45,000 mini excavator makes sense if your last eight jobs show you could have completed work three weeks faster with that equipment, directly translating to labor savings that exceed the equipment cost over two years.

Your bid strategy should shift based on what your completed jobs reveal about your true cost structure and margins. If your actual gross margins on jobs run 28 percent but you’re bidding at 32 percent, your pricing is disconnected from reality and you’re either underestimating costs or overestimating efficiency.

The Construction Financial Management Association reports that most builders should target net margins between 5 and 10 percent after overhead, which means your gross margin needs to absorb all indirect costs and still leave something for profit. Calculate what gross margin you actually need by working backward from your desired net margin. If you want 8 percent net profit and your overhead runs 18 percent of revenue, you need at least 26 percent gross margin to hit that target.

Any bid that won’t deliver that margin shouldn’t go out the door, no matter how much you want the work. Growth without this discipline destroys businesses because higher revenue with lower margins actually shrinks profit and strains cash flow. Before you bid aggressively to land bigger projects, protect your margins by confirming that your current jobs are delivering the margins your financial statements should show. If they aren’t, growing faster just means losing money faster.

Pull your last three completed jobs and compare actual labor hours, material costs, and timeline against what you estimated. Calculate your gross margin on each one, and if those numbers don’t match your expectations, that gap costs you money on every job you bid going forward. This exercise takes a few hours and often pays for itself within weeks through better pricing on your next project.

Commit to reviewing your financial statements for builders monthly instead of annually. Watch your days in accounts receivable, track labor and material variances on active jobs, and compare gross margins across projects so your financial data transforms from a historical record into an active management system. This rhythm protects your margins before they disappear, and most builders we work with at adding technology spot margin leaks they’ve been bleeding for years once they start this practice.

Building a stronger financial foundation doesn’t require hiring a full accounting department-it requires discipline, the right tools, and a willingness to act on what your numbers tell you. We at adding technology help construction companies streamline their financial processes and build real-time visibility into job costs and profitability, and whether you handle accounting internally or bring in outside support, the principle stays the same: understand your numbers, spot problems early, and let your financial statements guide your decisions.

At adding technology, we know you want to focus on what you do best as a contractor. In order to do that, you need a proactive back office crew who has financial expertise in your industry.

The problem is that managing and understanding key financial compliance details for your business is a distraction when you want to spend your time focused on building your business (and our collective future).

We understand that there is an art to what contractors do, and financial worries can disrupt the creative process and quality of work. We know that many contractors struggle with messy books, lack of realtime financial visibility, and the stress of compliance issues. These challenges can lead to frustration, overwhelm, and fear that distracts from their core business.

That's where we come in. We're not just accountants; we're part of your crew. We renovate your books, implement cutting-edge technology, and provide you with the real-time job costing and financial insights you need to make informed decisions. Our services are designed to give you peace of mind, allowing you to focus on what you do best - creating and building.

Here’s how we do it:

Schedule a conversation today, and in the meantime, download the Contractor’s Blueprint for Financial Success: A Step by-Step Guide to Maximizing Profits in Construction.” So you can stop worrying about accounting, technology, and compliance details and be free to hammer out success in the field.