Financial Controls for Builders: Strengthening Governance

Strengthen your construction company with financial controls for builders. Learn governance best practices to prevent fraud and improve accountability.

An audit doesn’t have to feel like a surprise inspection. When your financial records are organized and accurate, auditors move through their work smoothly, and you gain confidence in your numbers.

At adding technology, we’ve seen contractors who prepare year-round avoid costly corrections and stress. This guide walks you through what auditors actually look for and how to get your systems ready before they arrive.

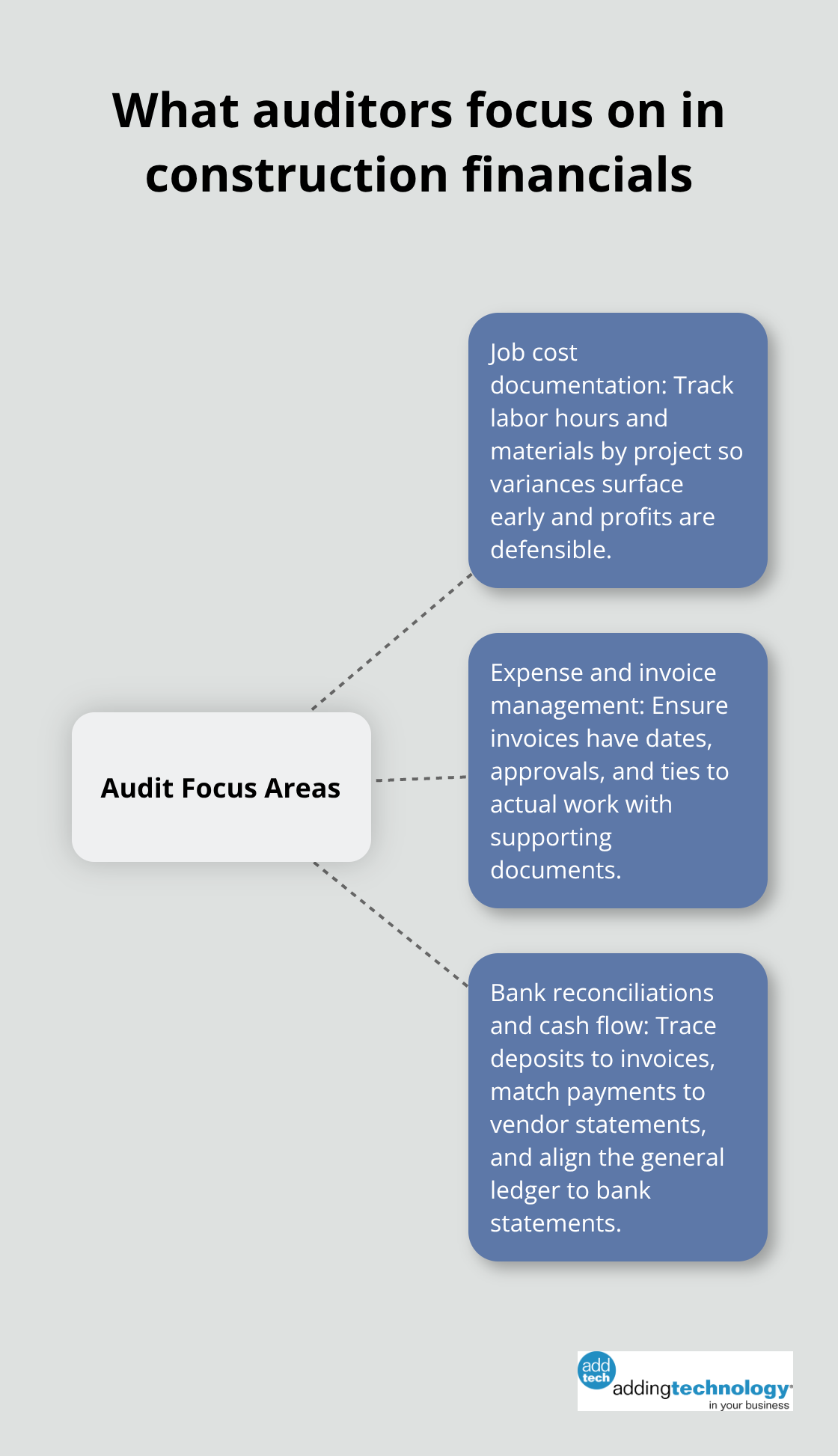

Auditors don’t show up to nitpick-they show up to verify that your financial records match reality. In construction, they focus on three areas that reveal whether your accounting system works or falls apart. Job cost documentation sits at the top of the list because auditors know that contractors who track labor and materials by project catch problems early. Without detailed job costing, you can’t defend your profit margins, and auditors will flag it immediately.

They want to see labor hours tied to specific jobs, material costs allocated correctly, and overhead distributed fairly across projects. If your timekeeping system doesn’t connect to job codes, or if materials land in a general account instead of assignment to projects, you’ll face questions that slow down the audit and raise doubt about your financial controls.

Expense records and invoice management come next, and this is where many contractors stumble. Auditors examine whether invoices carry dates, approvals, and ties to actual work performed. They look for missing documentation on transactions over certain thresholds. If you can’t produce a vendor invoice, a purchase order, or evidence that goods arrived, auditors will disallow the expense or require adjustments to your financial statements.

Bank reconciliations and cash flow records form the third pillar because cash doesn’t lie. Auditors trace deposits back to invoices, match payments to vendor statements, and verify that your general ledger matches your bank statements. Monthly reconciliations catch discrepancies early, but if you reconcile only at year-end, you hide problems that will surface during the audit. A clean reconciliation process shows auditors that your internal controls work and that someone actively monitors cash flow.

The stronger your documentation across these three areas, the faster the audit moves and the fewer adjustments you’ll face at the end. With these foundations in place, you’re ready to tackle the next critical step: organizing your financial systems so auditors find what they need without delay.

The gap between contractors who sail through audits and those who scramble often comes down to one thing: how early they organize their documentation. Most contractors wait until the audit notice arrives to hunt for receipts and invoices scattered across email, filing cabinets, and desk drawers. That approach costs time and creates stress. Treat documentation organization as a monthly task, not a year-end scramble. Start by designating one person as your financial record keeper-someone with clear responsibility for collecting and filing receipts, invoices, purchase orders, and vendor statements.

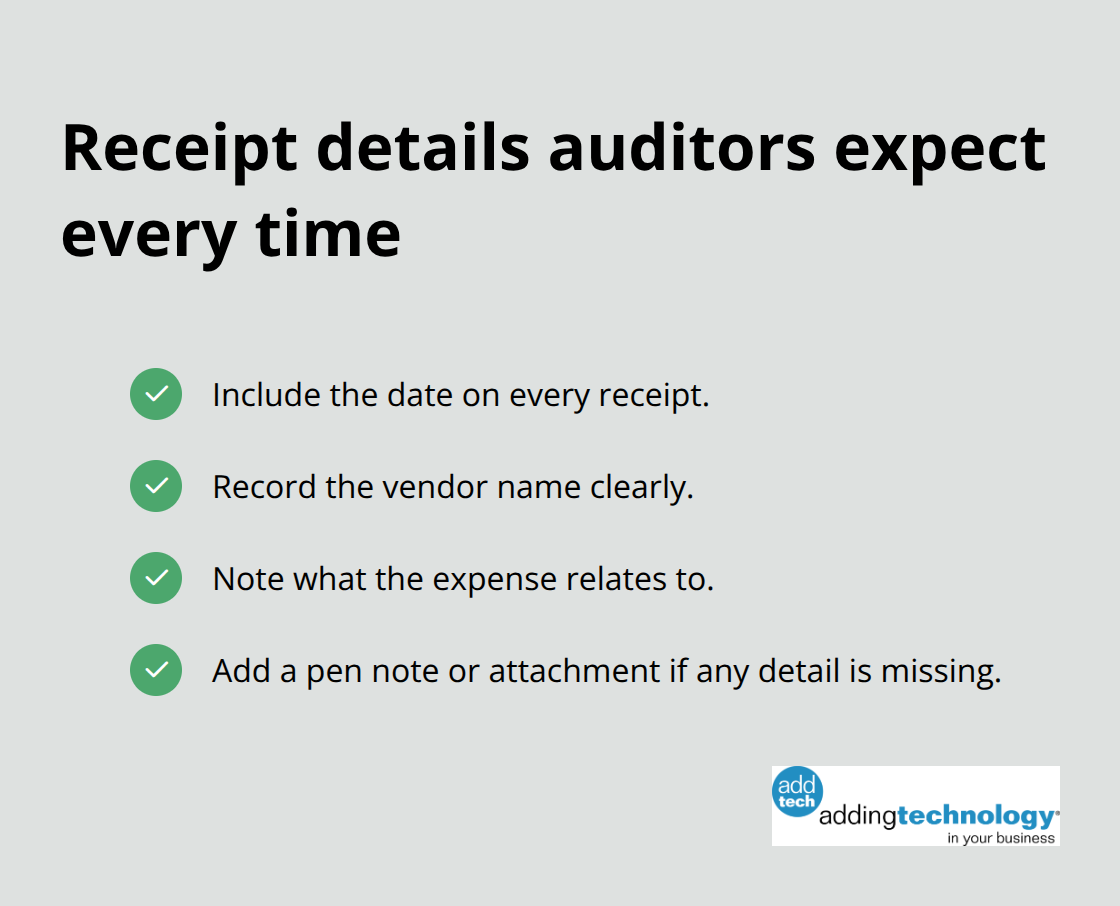

Create a simple folder structure, either physical or digital, that mirrors your chart of accounts or job codes. Every receipt needs three pieces of information: the date, the vendor name, and what the expense relates to.

If a receipt lacks any of these, ask your team to add them in pen or a note attached to the document. Monthly reconciliation catches misplaced items before they pile up. Set a specific day each month-ideally within five days of month-end-to pull all receipts, match them to your accounting software, and file them in order. This rhythm prevents the situation where you fall three months behind and can’t remember which invoice goes with which job.

Bank and credit card reconciliations deserve their own discipline because they reveal cash flow problems and accounting errors that auditors always investigate. Reconcile every account within five business days of the statement closing date, not weeks later when memory fades. Your goal is to match every deposit and withdrawal to your accounting records and identify any outstanding items. If a check hasn’t cleared after two weeks, follow up with the vendor. If a deposit appears in the bank but not in your records, investigate immediately-it might be a customer payment you forgot to invoice or a loan deposit that needs proper classification.

Payroll records demand the same attention because tax authorities and auditors scrutinize wage payments, withholdings, and payroll tax filings. Pull your payroll reports monthly and verify that gross wages match your job cost records and that all tax deposits hit on time. If you use a payroll processor, request a quarterly summary showing federal and state tax deposits, and cross-check those deposits against your bank statements. Auditors look for discrepancies between what you reported to the IRS and what your general ledger shows. Correct federal income tax withholding errors only if you discovered the errors in the same calendar year you paid the wages. Once these systems run smoothly, you’re positioned to spot the accounting mistakes that auditors flag most often-and that’s where your next focus should land.

Three mistakes appear so consistently in construction audits that auditors expect them. Misclassified expenses land in the wrong accounts, revenue gets recognized before work is truly complete, and job costs fail to tie back to actual labor and materials. Auditors flag these issues immediately because they distort your profit margins and confuse your financial picture.

Start with a clean chart of accounts that separates direct job costs from overhead, indirect labor, and administrative expenses. If your chart lumps everything together, you’ll spend the audit reclassifying entries and explaining why your numbers don’t match industry standards. A well-organized chart of accounts makes the audit move faster and gives you clearer visibility into which projects actually make money.

ASC 606 governs revenue recognition for construction, and it’s strict: you can’t record revenue from a change order until it’s approved and the amount is reasonably certain. Many contractors recognize revenue too early, especially on unpriced change orders or claims still under negotiation. Auditors will reverse those entries and demand supporting documentation showing customer approval and signed contracts.

Establish a formal process where change orders sit in a holding account until approved, then move to revenue only when conditions are met. Document every step with written approvals before work starts. This discipline prevents the costly adjustments that auditors impose when they find revenue recorded without proper authorization.

Job costing errors multiply quickly when labor hours aren’t tied to specific projects or when materials flow into general accounts instead of job codes. If a crew member works across three jobs in a week, your timekeeping system must track hours by job, not lump them together. The same applies to materials: a purchase order should reference the job it supports, and invoices should land in the correct job cost account.

Auditors request your work-in-progress reports monthly, and they reconcile those reports to your general ledger. If WIP doesn’t match the ledger, you face a lengthy investigation. Review cost-to-complete estimates with your project managers every month to catch margin erosion before year-end. If a project shows 60 percent complete but costs are running 75 percent of budget, investigate immediately.

Overhead allocation causes problems too, especially when contractors use only direct labor hours to spread overhead across jobs. Equipment-heavy projects absorb less overhead under that method, distorting true project profitability. Instead, allocate overhead using a blended approach that includes labor, equipment costs, or actual resource consumption (this might mean adjusting your allocation method quarterly as project mixes change).

Document your allocation method in writing so auditors understand your logic and can verify consistency across all projects. A documented, defensible overhead allocation method removes one of the most common audit questions and shows that you’ve thought through how your indirect costs actually flow to the work you perform.

Audit readiness for contractors rests on three core habits: organize your records monthly, reconcile your accounts on schedule, and document every decision that affects your financials. Start this month by assigning someone to own your documentation, building a filing system that matches your chart of accounts, and setting a calendar reminder for monthly reconciliations. These steps consume hours, not weeks, and they prevent the scramble that costs time and credibility when auditors arrive.

Being audit-ready year-round delivers benefits that extend far beyond passing an audit. Lenders and bonding companies trust contractors whose financials are clean and consistent. You gain real visibility into which projects actually profit, where costs run high, and where cash flow problems hide. Your team stops hunting for receipts and invoices, and your accounting closes faster each month.

If your current accounting setup lacks the structure to support real-time job costing, monthly WIP reconciliation, or automated bank matching, that’s the moment to upgrade. Adding Technology specializes in renovating accounting systems for construction contractors and implementing the advanced technology that removes manual burden from your team. Audit readiness isn’t a destination you reach once-it’s a rhythm you establish and maintain, and the right systems make that rhythm sustainable.

At adding technology, we know you want to focus on what you do best as a contractor. In order to do that, you need a proactive back office crew who has financial expertise in your industry.

The problem is that managing and understanding key financial compliance details for your business is a distraction when you want to spend your time focused on building your business (and our collective future).

We understand that there is an art to what contractors do, and financial worries can disrupt the creative process and quality of work. We know that many contractors struggle with messy books, lack of realtime financial visibility, and the stress of compliance issues. These challenges can lead to frustration, overwhelm, and fear that distracts from their core business.

That's where we come in. We're not just accountants; we're part of your crew. We renovate your books, implement cutting-edge technology, and provide you with the real-time job costing and financial insights you need to make informed decisions. Our services are designed to give you peace of mind, allowing you to focus on what you do best - creating and building.

Here’s how we do it:

Schedule a conversation today, and in the meantime, download the Contractor’s Blueprint for Financial Success: A Step by-Step Guide to Maximizing Profits in Construction.” So you can stop worrying about accounting, technology, and compliance details and be free to hammer out success in the field.