Financial Controls for Builders: Strengthening Governance

Strengthen your construction company with financial controls for builders. Learn governance best practices to prevent fraud and improve accountability.

Construction businesses face significant challenges when seeking project finance for construction ventures. Traditional funding methods often fall short of meeting the complex needs of modern building projects.

We at adding technology understand these financing hurdles firsthand. The right funding strategy can make the difference between project success and costly delays.

This guide provides proven methods to secure the capital your construction projects need to move forward.

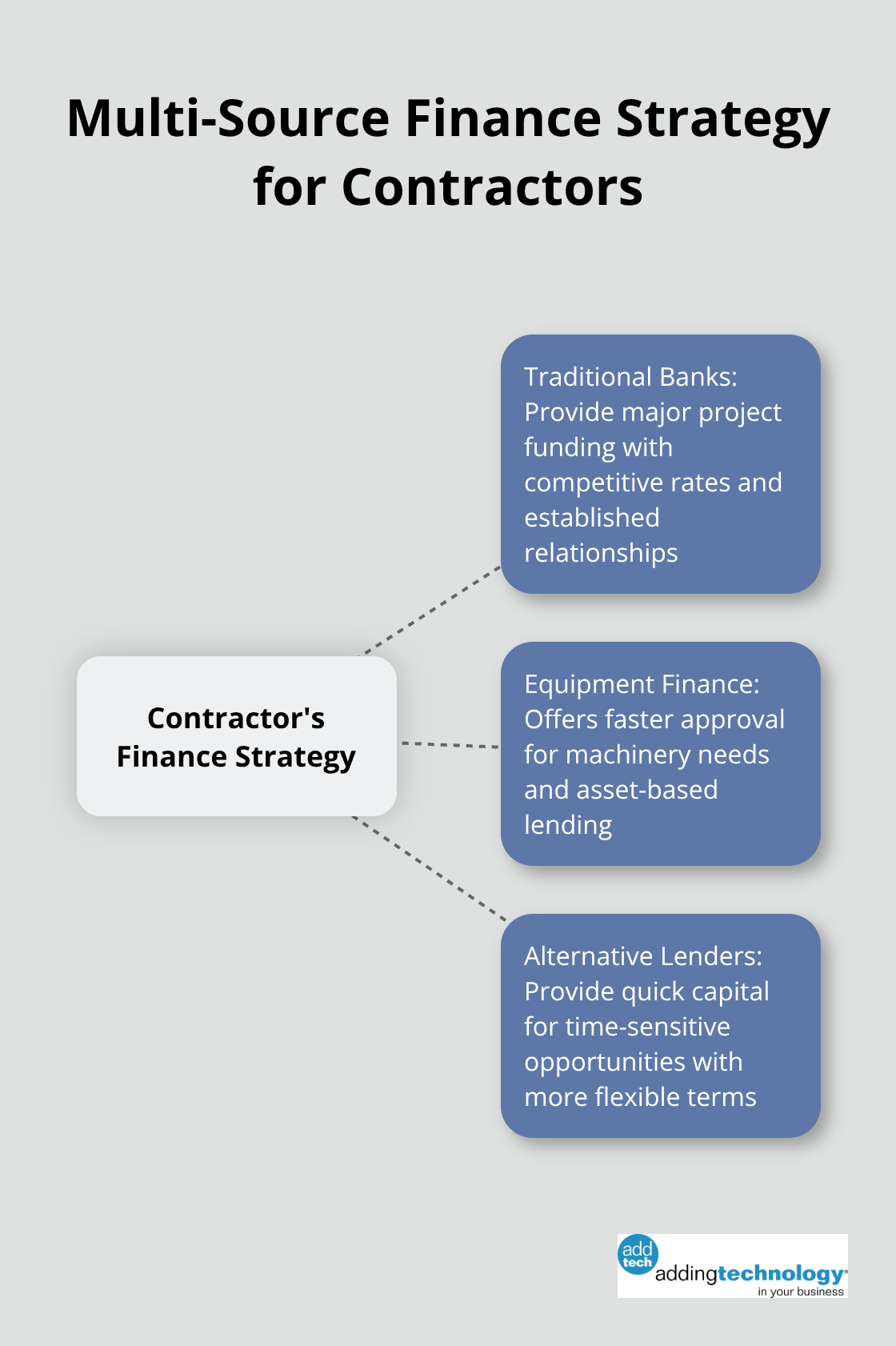

Construction projects demand flexible finance solutions that match project timelines and cash flow patterns. Banks still dominate the construction lending space, with commercial construction loans providing substantial financing for real estate development projects according to Federal Reserve data. These traditional loans offer competitive rates between 5.5% and 8.5% for established contractors with strong credit histories.

Banks require substantial documentation and typically take 45-90 days for approval. However, they provide the most cost-effective capital for major projects. Contractors with established relationships often secure better terms and faster processing times.

Equipment finance presents a faster alternative, with approval times that average 7-14 days and loan amounts that reach up to 90% of equipment value. Lenders focus on the asset value rather than extensive financial documentation, which speeds the approval process significantly.

Asset-based lending against existing equipment or receivables can provide working capital within weeks rather than months. This approach works particularly well for contractors who own valuable machinery but need immediate cash flow for new projects.

Private investors and alternative lenders have grown significantly, with construction lending making up about 15% of all new loans this year according to industry reports. These sources offer speed and flexibility but at higher costs, with rates often exceeding 12-15%.

Alternative lenders evaluate deals faster (often within 5-10 business days) and accept projects that traditional banks might reject. They prove valuable for time-sensitive opportunities or contractors with less established credit histories.

The most successful contractors maintain relationships with at least three different finance sources, which allows them to match funding type to project requirements and timeline constraints. Start with traditional bank relationships for major project funding, supplement with equipment finance for machinery needs, and maintain private investor connections for quick capital when opportunities arise.

This multi-source approach provides flexibility when market conditions change or when specific project requirements demand different finance structures. Your next step involves preparing the comprehensive documentation that lenders require to evaluate your projects effectively.

Financial institutions demand specific documentation that proves your construction business can repay loans and complete projects successfully. The approval process centers on three core document categories that lenders examine with mathematical precision.

Profit and loss statements from the past three years must show consistent revenue growth. Most lenders require annual revenues of at least $500,000 for significant project finance. Cash flow projections need monthly breakdowns for the next 18 months, and these must include seasonal variations that construction businesses typically experience.

Balance sheets must demonstrate positive equity ratios that meet regulatory capital requirements. Accounts receivable reports cannot show more than 15% of receivables older than 90 days (this signals collection problems that concern lenders). Your credit score needs to exceed 680 for competitive rates, while business credit reports must show payment histories with suppliers and subcontractors that span at least two years.

Detailed cost estimates separate successful applications from rejections. Lenders expect line-item breakdowns that account for materials, labor, equipment, and overhead expenses. Construction schedules must include milestone payments that align with project phases, typically structured as 20-30% down payment, 50-60% during construction phases, and final payment upon completion.

Timeline documentation should factor in weather delays and permit approval processes. Most lenders add 15-20% buffer time to contractor estimates because they know construction projects face unexpected delays. Your documentation package must present realistic timelines that account for these variables.

Lenders evaluate your completed project history and consider multiple factors including credit score, income, and cash flow when assessing portfolio loans. They prefer contractors who have completed similar project types and sizes. Client references from previous projects carry significant weight, particularly when they include payment completion confirmations and project delivery timelines.

Insurance certificates, bonding capacity, and professional licenses must remain current throughout the application process. These documents prove your business operates legally and maintains proper risk management protocols.

Strong financial documentation forms the foundation, but your approval chances improve dramatically when you implement specific strategies that address lender concerns about construction project risks.

Smart contractors establish relationships with at least three financial institutions during profitable periods, not when cash flow problems emerge. Community banks often provide more flexible terms for local contractors and maintain closer relationships with their business clients. Schedule quarterly meetings with loan officers to discuss your business performance and upcoming projects. Share financial statements proactively, even when you don’t need funds immediately.

Lenders remember contractors who communicate transparently about both successes and challenges. When you face project delays or cost overruns, inform your banking partners immediately rather than wait until loan payments become difficult. This approach builds trust that pays dividends when you need emergency funds or want to expand your credit lines.

Lenders reject construction loans primarily due to inadequate risk assessment, not insufficient collateral. Your application must address the five major risks that concern financial institutions: weather delays, labor shortages, material cost fluctuations, permit complications, and subcontractor failures. Document specific contingency plans for each risk category, including backup suppliers, alternative labor sources, and weather protection measures.

Professional liability insurance with minimum coverage requirements demonstrates serious risk management commitment. Performance bonds for projects that exceed $500,000 show lenders that surety companies have evaluated and approved your capabilities.

Advanced financial management systems provide the real-time data that lenders demand for approval decisions. Professional accounting services can renovate your financial systems to deliver accurate job costing and compliance documentation (which banks scrutinize carefully). These systems track project expenses, monitor cash flow patterns, and generate the detailed reports that separate approved applications from rejected ones.

Contractors who maintain professional financial oversight report improved approval rates and better loan terms. The investment in proper financial management pays for itself through lower interest rates and faster approval times.

Project finance for construction demands a strategic approach that combines multiple sources, comprehensive documentation, and strong lender relationships. Traditional bank loans provide the foundation with competitive rates, while equipment finance and alternative lenders fill specific gaps in your capital structure. Your success depends on detailed financial records, realistic project timelines, and transparent communication with financial partners.

Professional financial management systems separate approved applications from rejected ones by providing the real-time data and compliance documentation that lenders demand. The construction industry rewards contractors who invest in proper financial infrastructure. Adding Technology helps construction businesses achieve improved cost visibility and smoother operations through advanced financial management solutions.

Establish relationships with multiple lenders before you need capital, maintain professional financial oversight, and document your risk management strategies thoroughly. These steps position your construction business for sustainable growth and consistent access to the capital that drives project success. Strong financial foundations create opportunities for contractors who prepare properly and maintain professional standards (which banks recognize and reward with better terms).

At adding technology, we know you want to focus on what you do best as a contractor. In order to do that, you need a proactive back office crew who has financial expertise in your industry.

The problem is that managing and understanding key financial compliance details for your business is a distraction when you want to spend your time focused on building your business (and our collective future).

We understand that there is an art to what contractors do, and financial worries can disrupt the creative process and quality of work. We know that many contractors struggle with messy books, lack of realtime financial visibility, and the stress of compliance issues. These challenges can lead to frustration, overwhelm, and fear that distracts from their core business.

That's where we come in. We're not just accountants; we're part of your crew. We renovate your books, implement cutting-edge technology, and provide you with the real-time job costing and financial insights you need to make informed decisions. Our services are designed to give you peace of mind, allowing you to focus on what you do best - creating and building.

Here’s how we do it:

Schedule a conversation today, and in the meantime, download the Contractor’s Blueprint for Financial Success: A Step by-Step Guide to Maximizing Profits in Construction.” So you can stop worrying about accounting, technology, and compliance details and be free to hammer out success in the field.