Construction Compliance Checklist: Staying Auditable On Every Job

Track construction compliance requirements with our essential checklist to keep every job auditable and protect your business.

Construction companies live with constant financial uncertainty. Project payments arrive late, equipment breaks down unexpectedly, and market conditions shift without warning.

Short term cash reserves act as your buffer against these disruptions. At adding technology, we’ve seen firsthand how contractors with solid reserves weather storms that sink unprepared competitors. This guide shows you exactly how to build and protect the safety net your business needs.

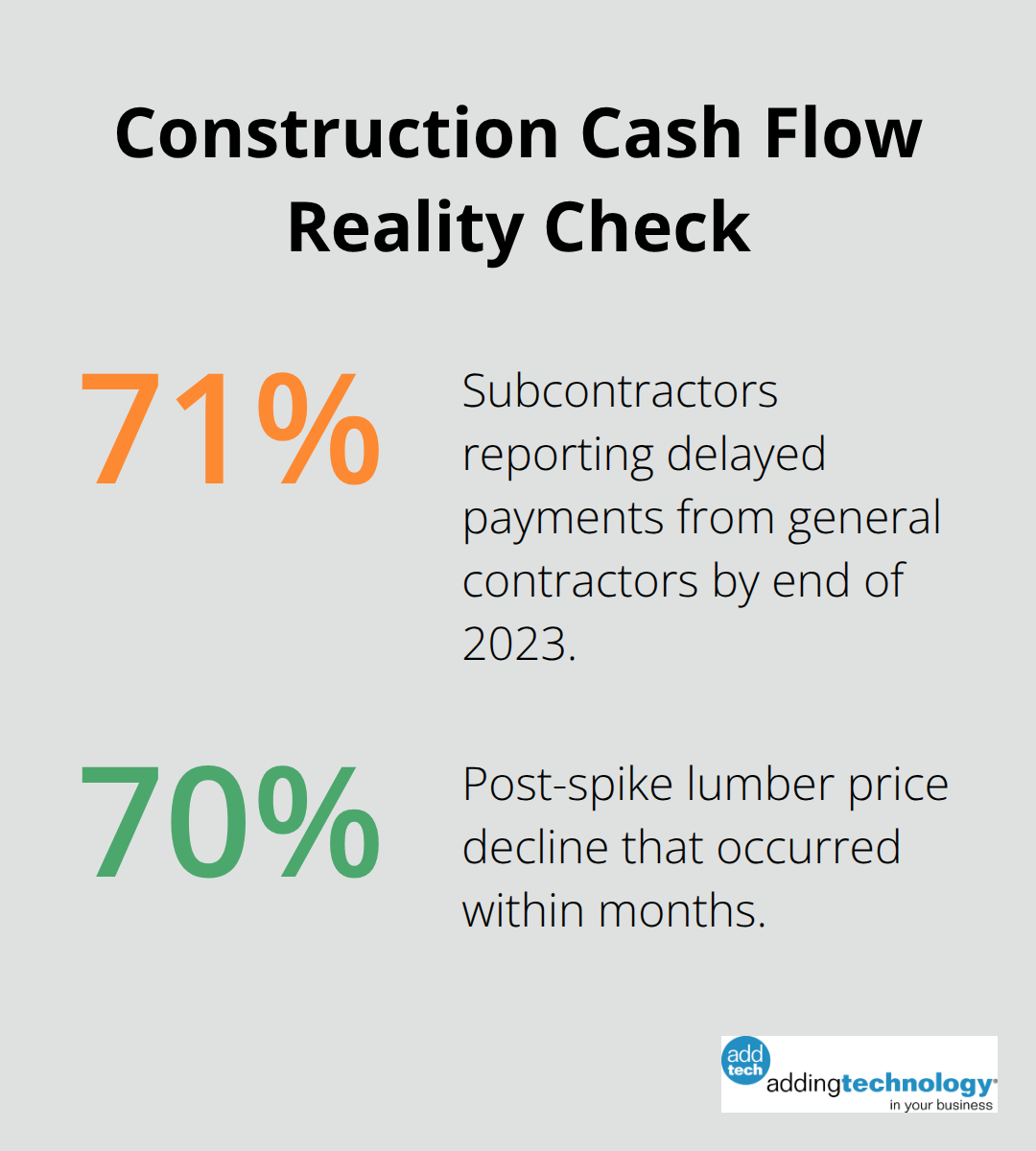

Late payments in the construction industry plague construction as a standard practice, not an exception. By the end of 2023, 71% of subcontractors reported delayed payments from general contractors. When a major client holds back a draw or stretches payment terms, your payroll obligations don’t pause. Your subcontractors demand payment on schedule.

Your equipment lease comes due regardless of whether you’ve collected from the job. Without reserves, you’re forced to borrow at unfavorable rates, skip payments to suppliers, or worse, miss payroll. Contractors who lose talented crews often cite cash flow delays that prevented timely paychecks as the breaking point. A three to six month operating reserve isn’t a luxury-it’s the difference between surviving a payment delay and spiraling into operational crisis.

Construction assets fail without warning and demand immediate response. A concrete pump breaks down mid-pour, costing thousands to repair or rent a replacement for the week. A dump truck transmission fails and sidelines a revenue-generating asset for two weeks. These disruptions consume 5 to 10% of annual operating expenses for many contractors. Without reserves, you either halt work, compromise project timelines, or tap expensive credit lines. Contractors who maintain solid reserves absorb these hits, keep crews productive, and protect client relationships. Those without reserves often face project delays that damage their reputation and eliminate future bid opportunities.

Construction contracts sharply when interest rates rise or lending tightens. Material costs spike unpredictably-lumber prices jumped 130% between 2020 and 2021, then fell 70% within months. Seasonal slowdowns in winter or during permit freezes stretch for months with minimal incoming revenue. Contractors without reserves during these periods cut corners, underbid work to generate cash, or close entirely. Those with adequate reserves maintain steady operations, invest in equipment upgrades when prices drop, and pursue strategic growth while competitors struggle. A reserve equal to four to six months of core expenses (payroll, insurance, equipment leases, and facility costs) provides the stability to navigate these cycles without desperation decisions that erode profitability.

The size and strength of your cash reserves determine how you respond when disruptions strike. Contractors with weak reserves react from panic-they accept unfavorable terms, skip maintenance that prevents larger failures, or sacrifice margins to keep cash flowing. Contractors with strong reserves respond from strategy-they track job profitability and negotiate better payment terms, invest in preventive maintenance, and make decisions based on long-term profitability rather than immediate survival. Building your target reserve amount requires understanding your specific operating expenses and committing to a realistic timeline.

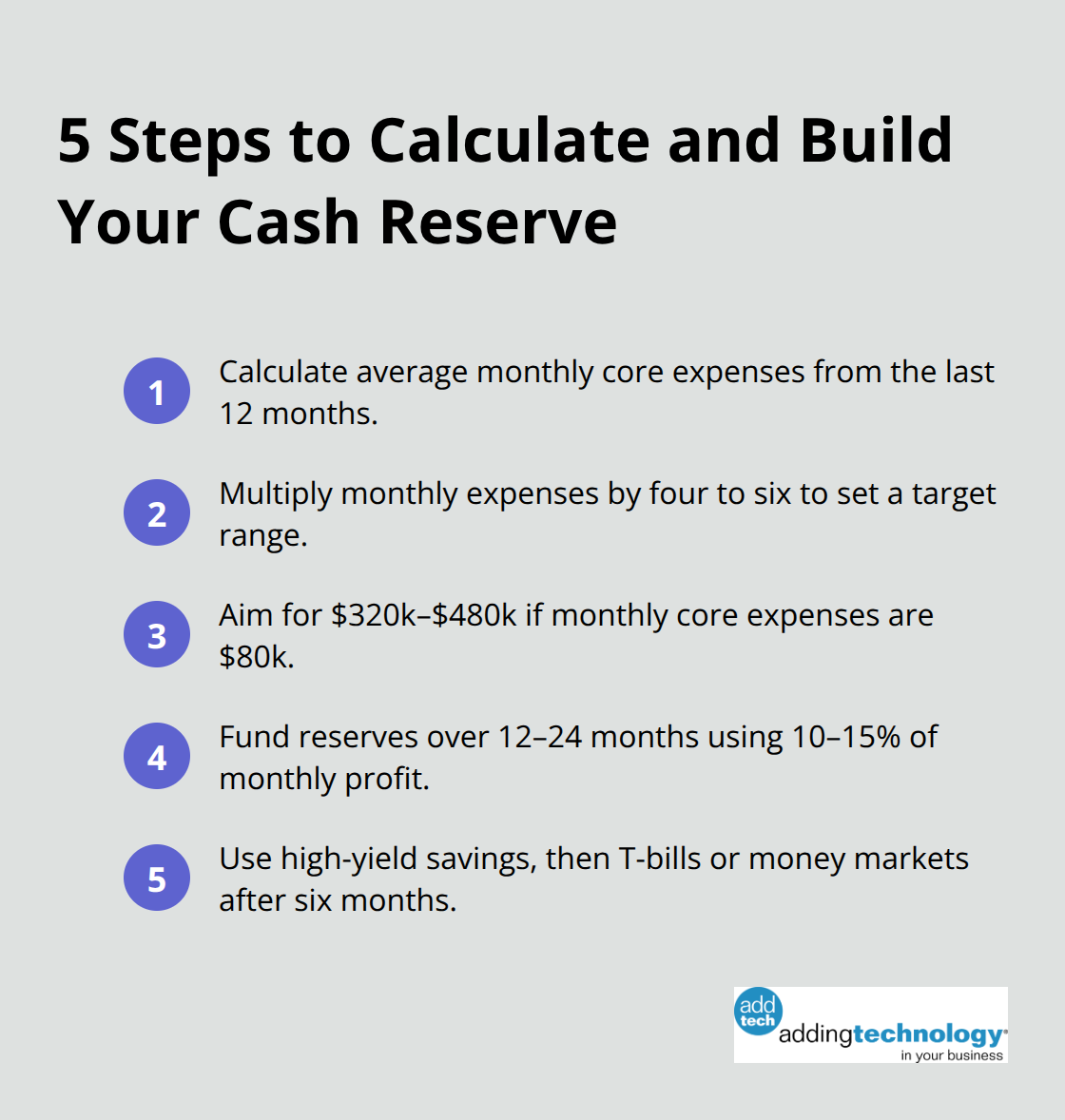

Pull your last twelve months of accounting records and identify what you actually spend each month on payroll, insurance, equipment leases, facility costs, utilities, and vehicle maintenance. Don’t estimate-use real numbers from your accounting software or bank statements. For construction companies, the sweet spot for operating expenses lies between 12-16% for general contractors and 15-25% for specialty contractors. This foundation determines everything that follows.

Once you know your monthly figure, multiply it by four to six months. This range covers extended payment delays, seasonal slowdowns, and unexpected equipment failures without forcing desperate decisions. A contractor with $80,000 in monthly core expenses needs a reserve between $320,000 and $480,000. This sounds large until you consider that a single major client payment delay of sixty days creates a $160,000 cash gap-your reserve bridges exactly these gaps.

Most contractors take twelve to twenty-four months to build adequate reserves, and that’s realistic. Start by redirecting 10% to 15% of monthly profit into a separate high-yield savings account (accounts currently pay between 4.5% and 5.3% annual interest, so your reserves earn money while they sit). After six months, move a portion into short-term Treasury bills or money market funds if you want slightly better returns without sacrificing liquidity.

Never mix reserve funds with your operating account because commingling makes it psychologically easier to spend emergency money on non-emergencies. Review your reserve level quarterly alongside your actual monthly expenses, because contractor costs shift seasonally and with project mix changes. A contractor experiencing growth adds equipment, hires staff, and increases insurance-pushing monthly expenses up 20% or more. Your reserve target adjusts accordingly. Track this in your accounting software so the numbers stay current and accurate.

With your target reserve calculated and a realistic funding timeline in place, the next step is protecting those reserves and keeping them separate from the daily cash flow demands of your business.

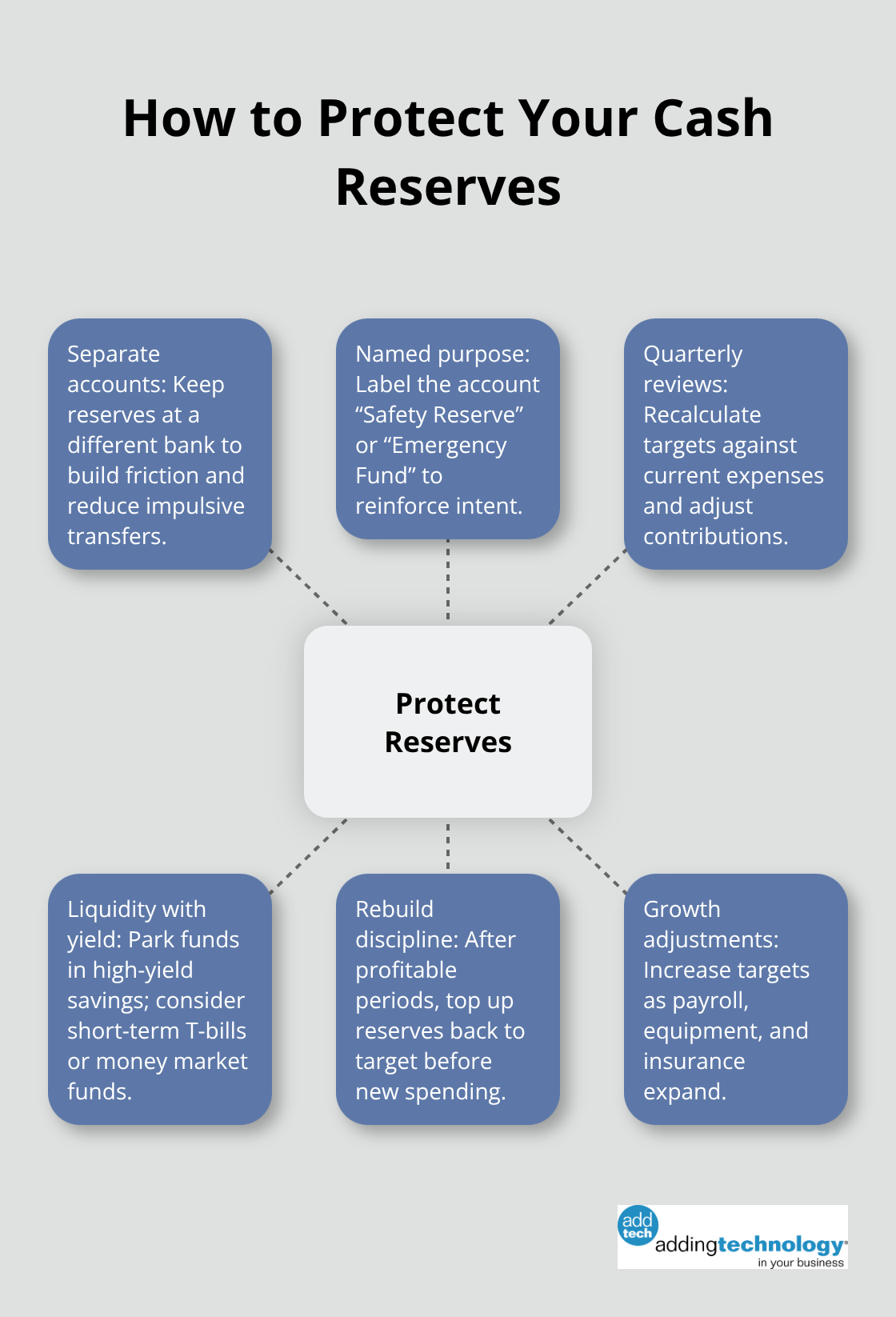

The moment you build a cash reserve, psychological pressure begins. A slow month arrives, payroll looms, and that reserve account suddenly looks like available cash to solve the problem. Contractors who fail at reserves don’t lack discipline-they fail because reserves sit in the same account as operating money, making the boundary invisible. The solution is ruthless account separation. Open a dedicated high-yield savings account at a different bank than your operating account-not the same bank, a different institution. This creates friction. Transferring money between banks takes one to two business days, which gives you time to reconsider whether the expense is truly urgent.

Name the account something specific like Safety Reserve or Emergency Fund, not something vague like Savings. When your accounting software shows that separate account with a clear balance, you resist the urge to rationalize spending it on payroll shortfalls or unexpected equipment costs that should come from operating cash flow. Some contractors use a certificate of deposit for a portion of reserves, accepting slightly lower interest rates in exchange for a maturity date that prevents casual withdrawals. This isn’t about losing access to the money in a crisis-it’s about making small emergencies solve themselves through tighter operating discipline rather than raiding the safety net.

Your reserve only works if you track it quarterly against current operating expenses, because your business isn’t static. Hire a new crew lead and your payroll jumps 8-12%. Expand into a new service line and insurance costs climb. Seasonal patterns shift, material costs fluctuate, and project mix changes. A contractor with $80,000 in monthly core expenses six months ago might now carry $95,000 after growth, meaning the $320,000 reserve that felt adequate is now undersized.

Review your actual monthly operating expenses each quarter using real numbers from your accounting software, then recalculate your target range. Most contractors find their reserve needs increase 5-15% annually as they grow. Track this in a simple spreadsheet or directly in your accounting system so the target stays current. When you complete a major project or experience a profitable quarter, redirect that surplus toward rebuilding reserves to their target level rather than spending it immediately. The discipline of quarterly review takes thirty minutes and prevents the slow erosion that leaves contractors underprepared when the next disruption hits.

Short term cash reserves transform how you operate as a contractor. The peace of mind that comes from knowing you can cover payroll during a payment delay, replace a failed piece of equipment, or weather a seasonal slowdown removes the constant financial anxiety that plagues underprepared businesses. Contractors with adequate reserves make decisions based on what’s best for long-term profitability rather than what keeps cash flowing today.

Start building your reserve today regardless of your company size. A solo operator with $20,000 in monthly expenses needs the same discipline as a twenty-person crew with $150,000 in monthly expenses. Redirect 10 to 15 percent of monthly profit into a separate account at a different bank, name it with intention, and treat it as untouchable except for genuine emergencies. After six months, move a portion into higher-yielding options like Treasury bills or money market funds.

Accounting software that shows your reserve balance alongside your operating account, real-time job costing that reveals which projects actually generate profit, and quarterly reviews that keep your target reserve aligned with current expenses transform short term cash reserves from a vague goal into a managed reality. Structured financial systems provide real-time visibility into cash flow, job profitability, and reserve levels so you can build and protect your safety net with confidence.

At adding technology, we know you want to focus on what you do best as a contractor. In order to do that, you need a proactive back office crew who has financial expertise in your industry.

The problem is that managing and understanding key financial compliance details for your business is a distraction when you want to spend your time focused on building your business (and our collective future).

We understand that there is an art to what contractors do, and financial worries can disrupt the creative process and quality of work. We know that many contractors struggle with messy books, lack of realtime financial visibility, and the stress of compliance issues. These challenges can lead to frustration, overwhelm, and fear that distracts from their core business.

That's where we come in. We're not just accountants; we're part of your crew. We renovate your books, implement cutting-edge technology, and provide you with the real-time job costing and financial insights you need to make informed decisions. Our services are designed to give you peace of mind, allowing you to focus on what you do best - creating and building.

Here’s how we do it:

Schedule a conversation today, and in the meantime, download the Contractor’s Blueprint for Financial Success: A Step by-Step Guide to Maximizing Profits in Construction.” So you can stop worrying about accounting, technology, and compliance details and be free to hammer out success in the field.