Construction Compliance Checklist: Staying Auditable On Every Job

Track construction compliance requirements with our essential checklist to keep every job auditable and protect your business.

Construction accounting for small contractors works differently than standard bookkeeping. You’re managing multiple projects at once, dealing with irregular cash flow, and tracking costs that shift week to week.

At adding technology, we’ve seen contractors lose thousands because they didn’t understand their true project profitability or cash position. This guide walks you through the accounting practices that actually matter for your business.

Construction accounting operates in a completely different financial universe than retail, services, or manufacturing. Your revenue doesn’t arrive in predictable monthly chunks. Your costs don’t follow a standard pattern. A single project can span months or years, with money flowing in and out at irregular intervals. Standard bookkeeping fails the moment you manage multiple active projects with different profitability levels, different payment schedules, and different cost structures. You need job costing to understand which projects actually make money and which ones drain your resources. Without it, you’re flying blind.

Most contractors price jobs based on estimates and historical data, but they never circle back to see what actually happened. That’s a massive mistake. Job costing tracks every dollar of labor, materials, equipment, and subcontractor costs tied directly to each project. When you run this data, you often discover that jobs you thought were profitable actually lost money, while others exceeded expectations.

The difference between margin and markup matters here-margin is your gross profit as a percentage of the sales price, while markup is a percentage over cost. Pricing mistakes in this distinction erode profits faster than you realize. Real-time tracking of committed costs like open subcontracts, purchase orders, and field time prevents budget overruns before they happen. Without visibility into these numbers, you make decisions based on incomplete information.

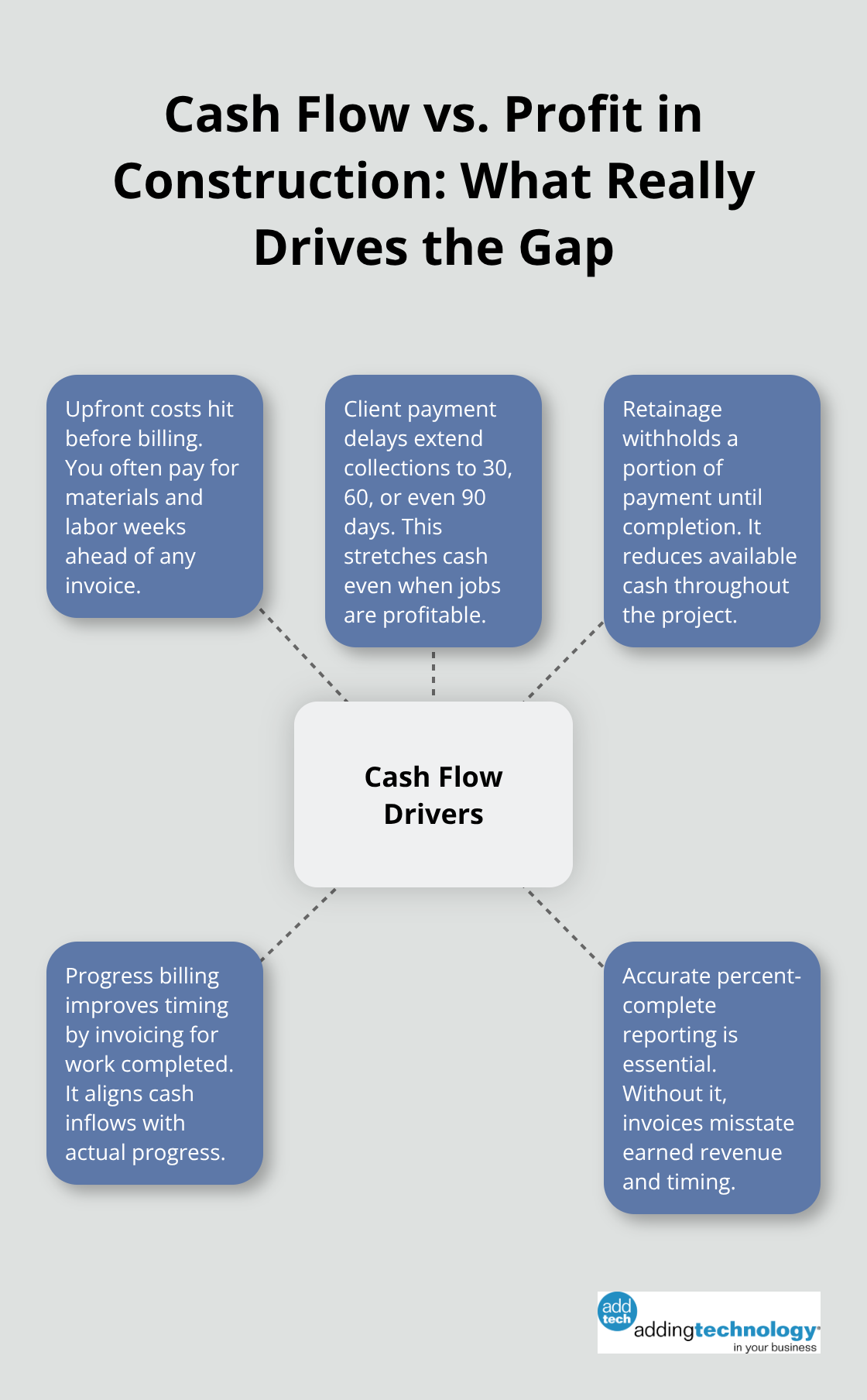

Construction creates a cash timing problem that other industries rarely face. You pay for materials and labor upfront, sometimes weeks before you bill the client. Then the client takes 30, 60, or even 90 days to pay-and that’s before retainage. Retainage is money the client holds back, released only at project completion. This means a profitable project can still starve your cash position.

A project that looks profitable on paper might require you to cover payroll and material costs from your own reserves. Progress billing helps here-you invoice based on work completed, not just work started. But you need accurate reporting to know what percentage of work is actually complete.

The difference between units complete, percent complete, and cost-to-finish methods matters because each one tells a different story about your project status. Track this wrong and you’ll either underbill (leaving money on the table) or overbill (creating false cash that evaporates when you complete the work).

Many contractors confuse overbilling with actual profit. Overbilling affects cash flow temporarily but isn’t real profit until the work is genuinely finished. This distinction shapes how you forecast your financial position and plan for upcoming expenses. Understanding your true cash position-not just what looks good on paper-determines whether you can cover payroll next week or whether you’ll need to tap a line of credit.

The financial reports you generate from this data become your roadmap for the next phase of your business.

Job costing reports are not optional-they separate contractors who know their profitability from those who guess. A proper job costing report tracks five critical data points: contract price, total cost estimate, actual cost-to-date, billed-to-date, and projected cost-to-finish. This combination tells you immediately whether a project tracks to budget or heads toward a loss.

Labor typically represents 30–40% of total project costs, so tracking hourly rates, benefits, and actual hours worked matters enormously. When you tie material purchases to specific cost codes as they occur, you prevent overruns and identify waste. Equipment costs (fuel, maintenance, and depreciation) must allocate to the correct job, whether equipment is owned or rented. Subcontractor costs need the same precision-labor, materials, and change orders should all track against the original contract to spot scope creep early.

Without this granular visibility, you make pricing decisions for future bids based on incomplete data, which perpetuates the cycle of unprofitable projects.

A project can show positive profit while your bank account empties because you paid vendors before invoicing clients. Cash flow statements expose this timing gap that profit reports mask. Track your committed costs-open subcontracts, open purchase orders, and field time-in real time so you know exactly what expenses arrive before they hit your payroll system.

Progress billing requires accurate work-in-progress reporting using your chosen method, whether units complete, percent complete, or cost-to-finish. Run WIP reports frequently (ideally monthly) to forecast whether you’ll meet budget and identify underbilling or overbilling situations before they become cash crises. This forward-looking visibility prevents surprises and keeps your operations stable.

Balance sheets show your true financial position-your assets, liabilities, and equity. Construction firms often overlook indirect costs like insurance, utilities, and administrative overhead when allocating expenses to jobs, which means your balance sheet looks stronger than it actually is. Set up a chart of accounts with standardized cost codes so every project uses the same categories for estimating, tracking, and reporting.

This common language across your business makes it far easier to compare performance between jobs and improve your bidding accuracy over time. When you allocate overhead and indirect costs to each project, you reveal true profitability per job rather than a distorted picture that hides money-losing work. These three reports-job costing, cash flow, and balance sheet-form the foundation for the next critical step: identifying and fixing the accounting mistakes that drain contractor profits.

The three most expensive mistakes we see contractors make don’t happen because they lack intelligence or effort. They happen because construction accounting gets messy fast, and most contractors use systems designed for retail or services, not project-based work.

The first killer mistake is mixing personal and business finances. When you pay yourself inconsistently, run personal expenses through the business account, or fail to separate owner draws from actual salary, your financial reports become worthless. You cannot accurately calculate job profitability if you don’t know your true labor costs, and you cannot know your true labor costs if personal withdrawals blur the line between business expenses and owner compensation.

Set up a separate business checking account, pay yourself a consistent salary or draw, and track every business expense through that account only. This single step transforms your ability to read your financial data and make decisions based on reality rather than confusion.

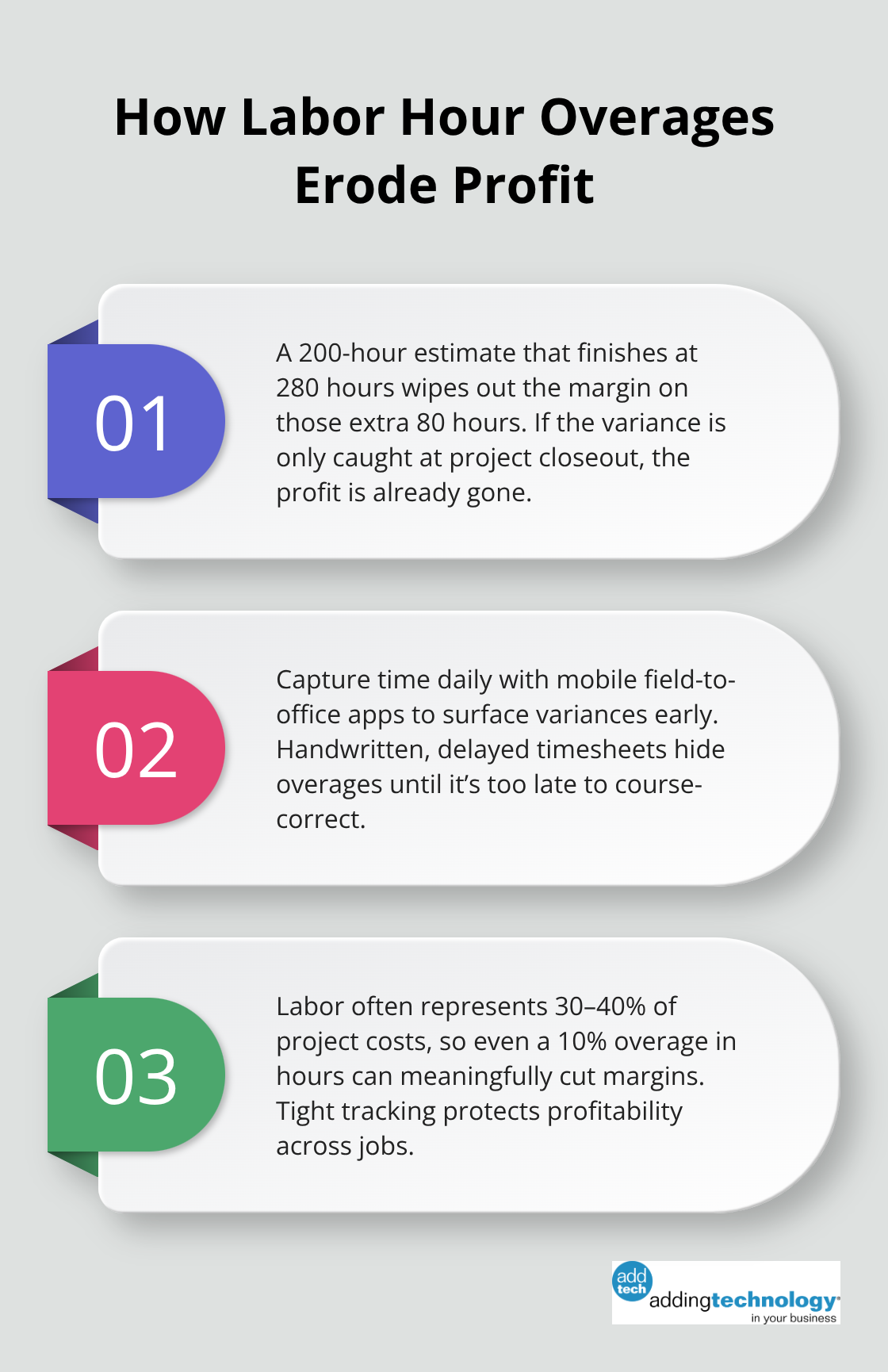

The second mistake costs contractors tens of thousands annually: failing to track actual labor hours against estimates. You estimate a job at 200 hours of labor, but your crew spends 280 hours. If you don’t catch this gap until the project ends, you’ve already lost the profit margin on 80 hours of work.

Require end-of-day time submissions from every crew member using mobile field-to-office apps, not handwritten timesheets that arrive days later. Track committed costs in real time so you see overages before they compound. Labor typically represents 30 to 40 percent of project costs, so a 10 percent overage on hours translates directly to significant profit loss.

The third mistake treats equipment as an expense rather than an asset with ongoing costs. You own an excavator, but you fail to allocate overhead expenses-such as insurance, equipment depreciation, and maintenance-to the specific projects using that equipment. This distorts your job profitability reports and makes you think unprofitable projects are breaking even.

Equipment costs include depreciation, insurance, and maintenance, and each dollar must attach to the correct job. When you neglect this allocation, you underbid future similar work based on incomplete cost data, perpetuating the cycle of low-margin projects.

These three mistakes share a common thread: they all create a gap between what your financial reports show and what actually happened on your jobs. Closing that gap requires discipline in data entry, real-time visibility into costs, and a chart of accounts that forces accurate categorization from day one.

Construction accounting for small contractors transforms from overwhelming to manageable once you implement the right systems. You now understand why standard bookkeeping fails, which reports matter most, and which mistakes drain your profits fastest. The path forward requires you to implement job costing, track labor hours in real time, allocate equipment costs accurately, and separate personal finances from business operations.

These practices reveal exactly where every dollar goes instead of forcing you to guess whether a project made money. You’ll forecast cash flow with confidence rather than wondering if you can cover payroll next week. You’ll base future estimates on actual project data instead of repeating the same pricing mistakes that undermine your margins. Adding technology helps contractors implement real-time job costing so you gain the visibility you need without the complexity.

Your construction business deserves a financial foundation as solid as the work you build. Start with one practice this month, add another next month, and watch how clarity transforms your decision-making and your bottom line.

At adding technology, we know you want to focus on what you do best as a contractor. In order to do that, you need a proactive back office crew who has financial expertise in your industry.

The problem is that managing and understanding key financial compliance details for your business is a distraction when you want to spend your time focused on building your business (and our collective future).

We understand that there is an art to what contractors do, and financial worries can disrupt the creative process and quality of work. We know that many contractors struggle with messy books, lack of realtime financial visibility, and the stress of compliance issues. These challenges can lead to frustration, overwhelm, and fear that distracts from their core business.

That's where we come in. We're not just accountants; we're part of your crew. We renovate your books, implement cutting-edge technology, and provide you with the real-time job costing and financial insights you need to make informed decisions. Our services are designed to give you peace of mind, allowing you to focus on what you do best - creating and building.

Here’s how we do it:

Schedule a conversation today, and in the meantime, download the Contractor’s Blueprint for Financial Success: A Step by-Step Guide to Maximizing Profits in Construction.” So you can stop worrying about accounting, technology, and compliance details and be free to hammer out success in the field.