How Contractors Can Improve Cash Flow Between Construction Projects

Improve cash flow between projects with practical strategies contractors can implement immediately to strengthen finances and reduce cash gaps.

Research projects fail financially more often than they succeed. Poor budgeting is the main culprit-most teams either underestimate costs or miss hidden expenses entirely.

At adding technology, we’ve seen firsthand how a solid research project budget template prevents these disasters. This guide walks you through building one that actually works.

Personnel costs consume 40 to 60 percent of most research budgets, and this is where teams make their first mistake. They list salaries but forget the associated costs that come with employing people. Fringe benefits-health insurance, payroll taxes, and retirement contributions-typically run 25 to 35 percent on top of base salary according to NIH guidelines. If a researcher earns $80,000 annually and you budget only the salary, you’ve already underfunded the project by $20,000 to $28,000.

The Personnel tab in most budget templates calculates these automatically, but only if you input the correct fringe rate from your institution. Equipment purchases above $5,000 with a service life exceeding one year require itemization and justification with price quotes. General-purpose equipment like computers often gets charged to overhead rather than directly to the project, which surprises many first-time budgeters.

Materials and supplies vary wildly depending on your research type, but most teams treat this as a lump sum rather than breaking it down by category. Software costs demand special attention because the threshold differs from physical equipment-most sponsors treat software above $100,000 as a capital asset. Travel budgets must specify destination, number of travelers, dates, and direct relevance to the research. Domestic travel should never exceed coach airfare rates, and international travel requires explicit sponsor approval before you include it.

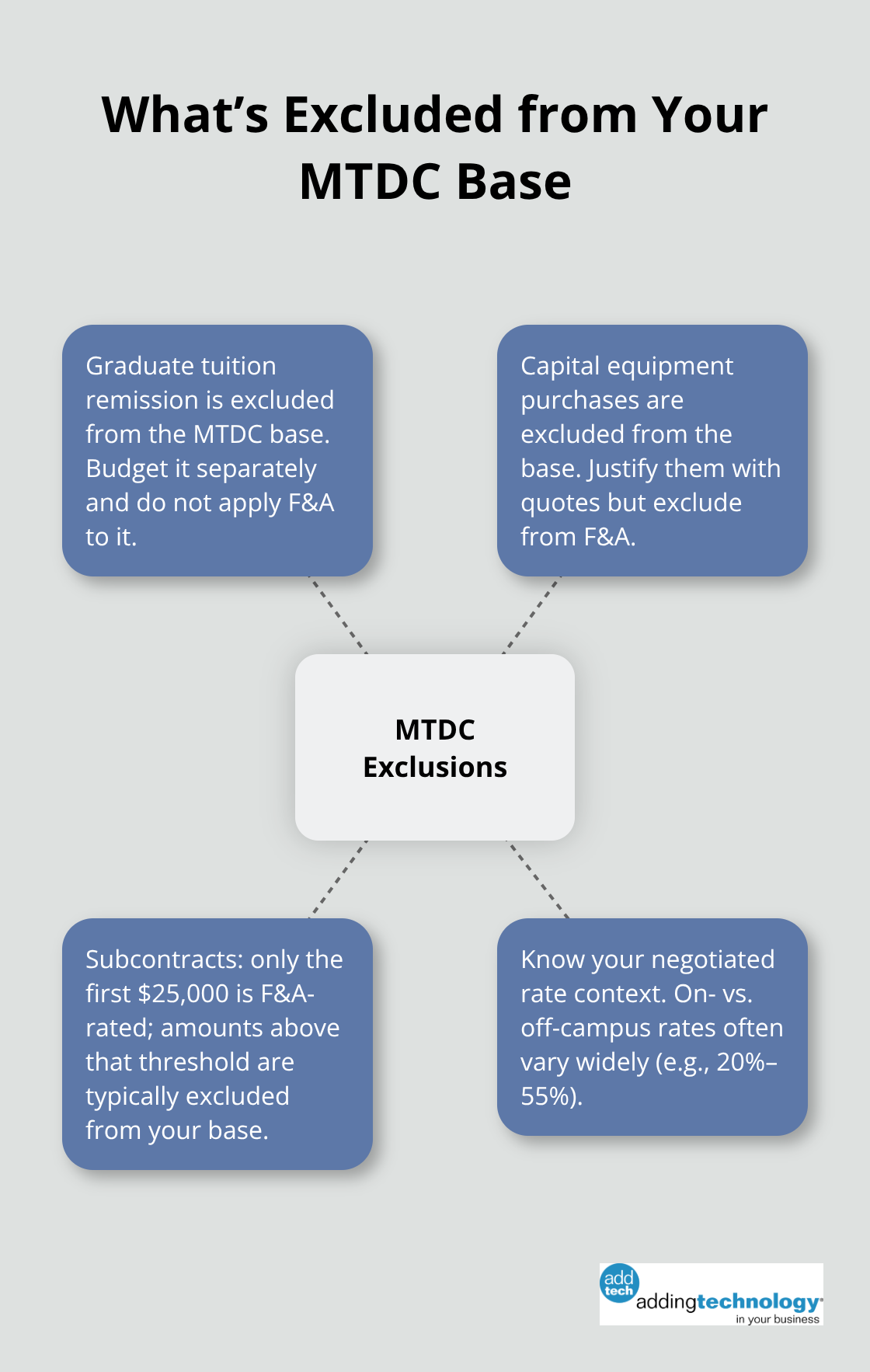

Indirect costs, also called facilities and administrative costs or F&A, are calculated as a percentage of your direct cost base. Your institution negotiates these rates with federal agencies, and rates typically range from 20 to 55 percent depending on whether your work happens on campus or off campus. The critical detail most researchers miss is understanding what counts in the direct cost base.

Graduate tuition remission, equipment purchases, and large subcontract charges get excluded from the MTDC base used for calculating F&A. If you work with subcontractors, the first $25,000 of each subcontract is F&A-rated, but amounts exceeding that threshold may be treated differently. The University of British Columbia illustrates two approaches: the Price Model embeds overhead into each line item, while the Cost Model lists overhead as a separate line item. With a 25 percent indirect rate, $201,000 in direct costs totals $251,250 when overhead is added separately.

A contingency reserve protects against cost escalation, but padding your budget with unnecessary contingency amounts signals poor planning to reviewers. Most sponsors allow contingency only for specific, predictable increases like inflation. Plan for out-year cost escalation by applying reasonable percentage increases-typically 2 to 3 percent annually for personnel and 3 to 5 percent for materials. Document major year-to-year variations in your budget justification and explain what drives them.

If your project spans multiple years, misaligning person-months with proposed methods becomes obvious to reviewers, so tie every salary allocation directly to specific project tasks. Gather current salary and benefit rates before you start building your template, and verify equipment and service costs with quotes from vendors rather than estimates. Understanding which cost model your sponsor requires prevents budget rejections during the review stage and positions you to move forward with confidence into the structural decisions that shape your entire template.

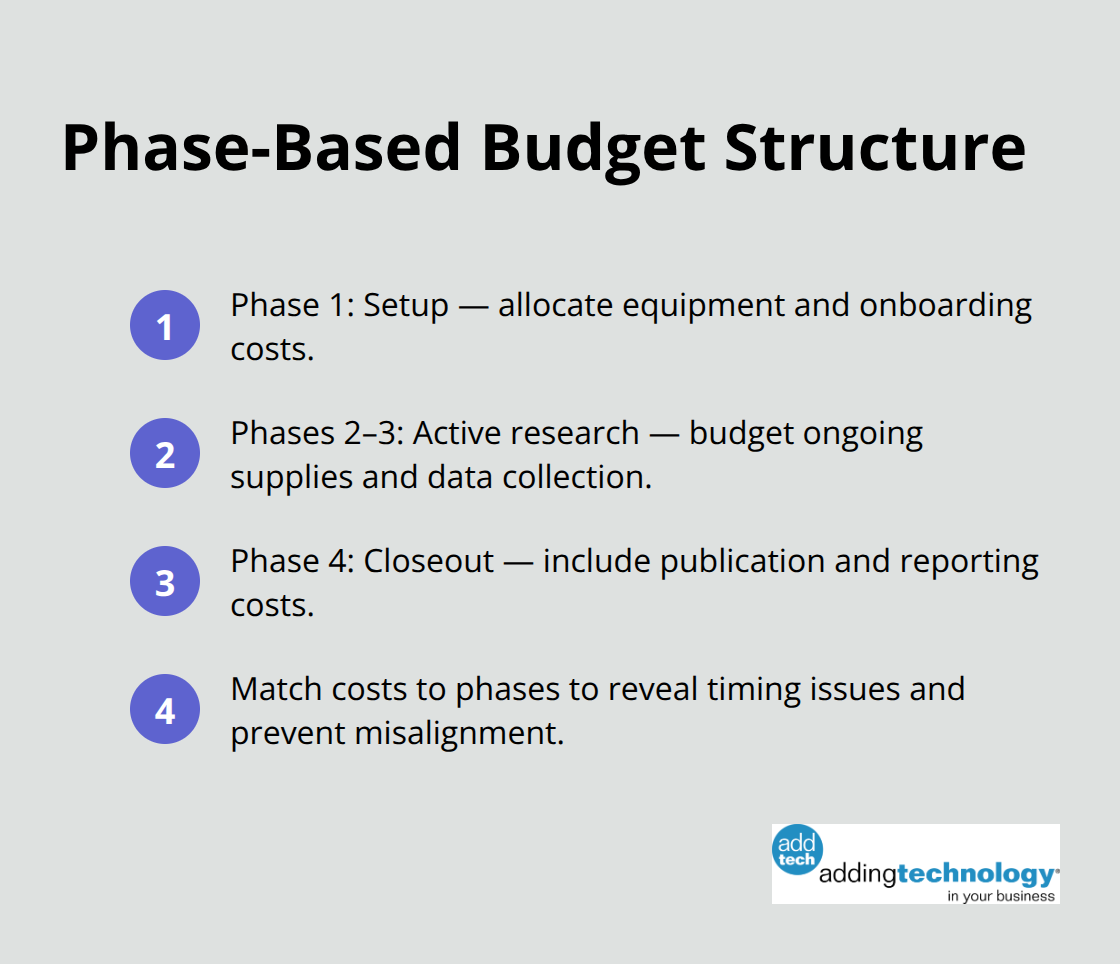

Start with the project timeline and work backward. You need to map every phase of your research from kickoff through final reporting, then assign costs to each phase rather than treating the budget as one monolithic number. This approach forces you to think about when money actually gets spent. A three-year research project that front-loads equipment purchases in year one looks fundamentally different from one that spreads technology investments across all three years. Most budget templates fail because they ignore this timing reality. When you structure by phase, you immediately spot problems like paying for personnel before the project officially starts or purchasing consumables after the research ends.

Reviewers evaluate whether your timeline matches your spending pattern, and misalignment signals poor planning. The NIH Grants Policy Statement emphasizes that budgets must reflect the actual sequencing of work, not just total dollar amounts. You should break your project into discrete phases-setup, active research, analysis, and closeout-and assign specific cost categories to each. Equipment goes in phase one, ongoing supplies in phases two and three, and publication costs in phase four. This structure also helps you identify which costs are truly variable versus fixed across all phases.

Line items are where most budgets go wrong because teams either create too many meaningless rows or lump everything into vague categories. Each line item should represent a distinct cost with a specific quantity and unit price that you can defend with documentation. Rather than writing Equipment: $50,000, specify Lab Centrifuge (1 unit at $28,000 with vendor quote attached), Microscope (1 unit at $15,000 with vendor quote), and Incubator (1 unit at $7,000 with vendor quote). This granularity matters because sponsors reject budgets with unexplained line items, and your institution’s grants specialist will request clarification on anything vague.

Line items with vendor quotes and documentation should include the necessity and suitability of the equipment, description, unit cost, and any quoted discount. Personnel line items need equal precision-state the researcher’s name, title, effort percentage, annual salary, and the specific project tasks they’ll perform. Graduate Research Assistants require special attention since tuition remission typically equals 50 percent of tuition costs and gets charged separately from stipend.

If your research extends beyond the initial budget period, you must plan for cost escalation explicitly. Personnel typically increases 2 to 3 percent annually according to NIH guidelines, while materials and supplies escalate 3 to 5 percent annually depending on category. Document these assumptions in your budget justification so reviewers understand your escalation logic.

Contingency reserves should never exceed 5 percent of total direct costs, and only then for projects with genuine uncertainty in subcontractor pricing or equipment availability. Padding your budget with unnecessary contingency signals to reviewers that you haven’t done adequate planning. Your next step involves identifying which mistakes most commonly derail budgets during the review process-and how to avoid them before your proposal reaches a sponsor’s desk.

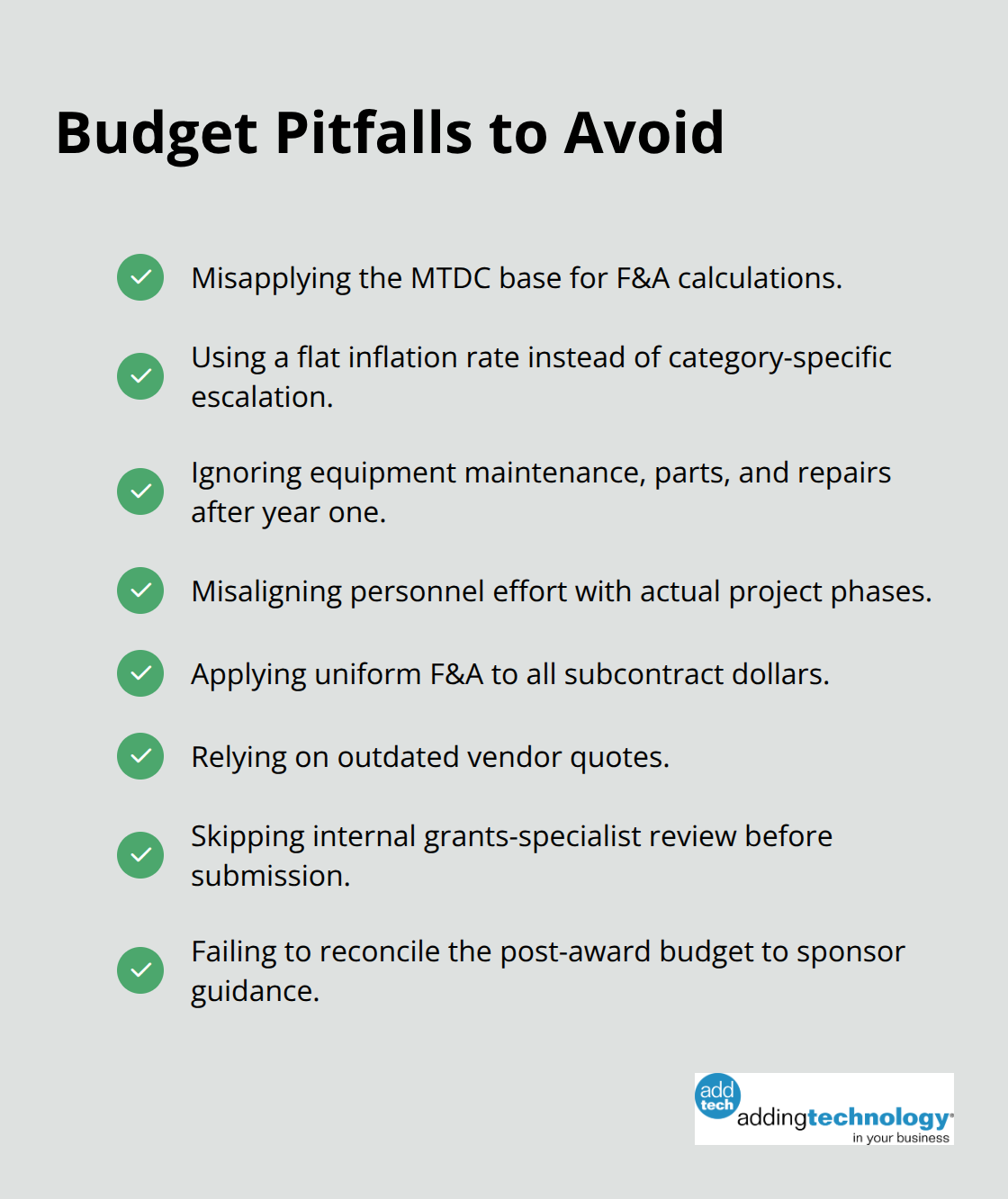

Most research budgets fail not because the math is wrong, but because researchers forget entire cost categories exist. Indirect costs represent the most frequent casualty. You calculate your direct costs meticulously, then apply your institution’s F&A rate to the direct cost base-except you’ve excluded graduate tuition, equipment over $5,000, and the first $25,000 of subcontract costs from that base without realizing it. The result: you’ve systematically underfunded overhead by 15 to 30 percent. NIH policy specifically excludes these items from the Modified Total Direct Cost (MTDC) base, yet researchers routinely treat their entire direct cost total as F&A-eligible. A $400,000 project with $150,000 in equipment and $80,000 in graduate tuition remission should calculate F&A on roughly $170,000 in remaining direct costs, not $400,000. That difference-potentially $54,000 to $99,000 depending on your F&A rate-appears nowhere in budgets that miss this detail.

Inflation compounds the damage across multi-year projects. You cannot simply apply a flat 2 percent increase across all line items and expect accuracy. Personnel typically escalates 2 to 3 percent annually according to NIH guidelines, but specialized equipment maintenance contracts often jump 4 to 6 percent yearly, and certain reagents or materials can spike 8 to 12 percent annually depending on commodity markets. A three-year project budgeting $50,000 annually for supplies without accounting for differential escalation by category will exhaust that line item by year two. Worse, many researchers never update their budgets after submission. Sponsor-awarded amounts frequently differ from requested amounts, particularly when F&A calculations get adjusted post-award or when direct cost caps force reductions. Your original budget template becomes obsolete the moment you receive the award letter, yet most teams continue spending against the outdated document rather than reconciling actual allocations against sponsor guidance.

Equipment purchased in year one depreciates and requires maintenance in years two and three, but most budget templates treat equipment as a one-time expense with no follow-up costs. If you budget $80,000 for a laboratory centrifuge in year one, you need service contracts ($3,000 to $5,000 annually), replacement parts ($1,500 to $2,500 annually), and eventual repairs that accelerate as equipment ages. Ignoring these secondary costs creates a false economy where year-one spending looks reasonable but years two and three become underfunded.

Personnel effort allocations often misalign with actual project phases. You allocate 50 percent effort to a senior researcher for all three years, but the actual work pattern might demand 80 percent in year one during setup and analysis, then 30 percent in year three during closeout and publication. Your budget shows consistent spending that doesn’t match reality, and reviewers catch this mismatch instantly. The solution requires mapping your project timeline first, then assigning costs to specific phases rather than distributing them evenly across years. A project front-loading equipment in year one looks fundamentally different from one spreading technology investments across all three years, and your budget must reflect this truth.

Subcontractors introduce complexity that catches most first-time budgeters off guard. The first $25,000 of each subcontract is F&A-rated at your institution’s rate, but amounts exceeding that threshold may be treated as a separate cost pool or excluded from your MTDC base entirely-the treatment varies by sponsor and institution. If you subcontract $80,000 worth of specialized analysis to an external lab, only $25,000 receives your F&A rate applied. The remaining $55,000 may have its own F&A rate from that institution baked in, or it might be treated as a direct pass-through cost. Most budgets ignore this distinction and apply uniform F&A calculations across all subcontract dollars, inflating your total by 5 to 15 percent.

Gathering current vendor quotes before budget submission prevents catastrophic underestimation. A $15,000 equipment estimate from a 2024 price list becomes obsolete by 2026 when you actually purchase. Technology costs shift particularly fast-software licensing that cost $5,000 annually five years ago might now demand $7,500 to $8,500 with subscription model changes. Obtain written quotes within 60 days of submission, not from memory or outdated catalogs. Your institution’s grants specialist should review your completed budget before it goes to the sponsor, catching indirect cost errors, missing line items, and unrealistic escalation assumptions. This internal review step prevents rejection and revision cycles that delay funding by months.

A research project budget template succeeds when it accounts for every cost category, applies realistic escalation rates, and receives review before submission. Personnel costs with accurate fringe rates, equipment with vendor quotes and maintenance plans, materials broken down by category with differential inflation assumptions, and indirect costs calculated against the correct direct cost base form the essential foundation. Your budget must reflect your actual project timeline and spending pattern rather than distributing costs evenly across years when reality demands front-loading or back-loading specific categories.

After your sponsor awards funding, reconcile the awarded amount against your original research project budget template and adjust allocations to match sponsor guidance and any cost caps they imposed. Review your budget quarterly against actual spending to catch escalation surprises early, and update your forecast immediately when equipment maintenance costs exceed projections or personnel effort shifts. Gather current vendor quotes at least every 12 months for major equipment or services, since technology costs shift rapidly and outdated pricing creates systematic underestimation.

Your institution’s grants specialist and finance team catch indirect cost calculation errors, identify missing line items, and flag unrealistic assumptions that reviewers will question before rejection occurs. For construction-related research or projects involving facility renovations and cost tracking, Adding Technology provides financial management services that streamline accounting systems and enable real-time job costing throughout your project lifecycle.

At adding technology, we know you want to focus on what you do best as a contractor. In order to do that, you need a proactive back office crew who has financial expertise in your industry.

The problem is that managing and understanding key financial compliance details for your business is a distraction when you want to spend your time focused on building your business (and our collective future).

We understand that there is an art to what contractors do, and financial worries can disrupt the creative process and quality of work. We know that many contractors struggle with messy books, lack of realtime financial visibility, and the stress of compliance issues. These challenges can lead to frustration, overwhelm, and fear that distracts from their core business.

That's where we come in. We're not just accountants; we're part of your crew. We renovate your books, implement cutting-edge technology, and provide you with the real-time job costing and financial insights you need to make informed decisions. Our services are designed to give you peace of mind, allowing you to focus on what you do best - creating and building.

Here’s how we do it:

Schedule a conversation today, and in the meantime, download the Contractor’s Blueprint for Financial Success: A Step by-Step Guide to Maximizing Profits in Construction.” So you can stop worrying about accounting, technology, and compliance details and be free to hammer out success in the field.