Compliance Training for Contractors: Staying Ahead of Regulations

Master compliance training for contractors with essential regulations and best practices to protect your business and team.

Most construction business owners leave thousands of dollars on the table every year. Tax deductions slip through the cracks, income timing gets overlooked, and cash flow suffers as a result.

At adding technology, we’ve seen contractors transform their bottom line by implementing smart construction tax planning strategies. The difference between a reactive approach and a strategic one can mean tens of thousands of dollars in your pocket.

Equipment sitting on your job site costs money every single day. That excavator, that skid steer, those power tools-they depreciate, and the tax code gives you multiple ways to write off that depreciation. Most contractors know depreciation exists, but they miss the accelerated methods that put cash back in your pocket this year, not over a decade.

In 2026, bonus depreciation allows 100% deduction on qualifying property placed in service by December 31, meaning a $50,000 piece of equipment becomes fully deductible immediately rather than spread across years. Section 179 adds another $2.56 million in deduction capacity for 2026, with the phase-out threshold at $4.09 million. Heavy machinery like excavators, bulldozers, backhoes, and skid steers all qualify. Work trucks over 6,000 pounds GVWR receive favorable treatment too-a $75,000 heavy-duty pickup becomes fully deductible in the purchase year under Section 179.

The catch matters: the equipment must actually be placed in service and actively used in your business by year-end. Many contractors wait until January to order equipment, missing the current-year deduction window entirely.

Your vehicle mileage to job sites, supplier meetings, and trade shows generates deductions at 72.5 cents per mile for 2026. You can also track actual expenses like fuel, maintenance, and insurance instead. Contractors who only claim the standard mileage rate often miss the actual expense method, which produces larger deductions when vehicles see heavy use.

Home office space used regularly for business administration qualifies for deductions too. A portion of mortgage interest or rent, utilities, internet, and homeowners insurance reduces your taxable income. If you run payroll from a dedicated home office, document it thoroughly.

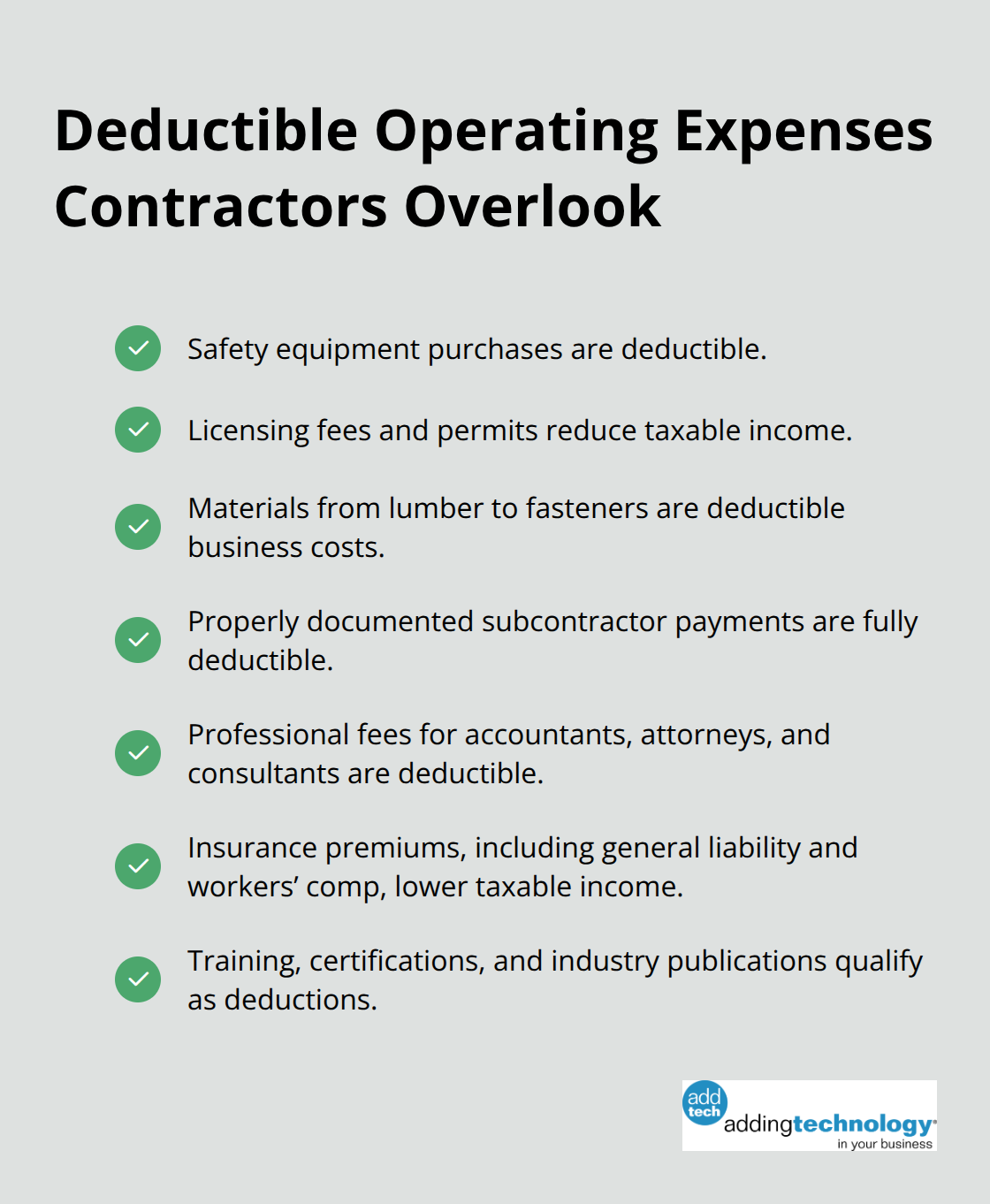

Safety equipment, licensing fees, permits, and materials from lumber to fasteners all count as deductible business expenses that slip past many contractors during year-end reconciliation. Subcontractor payments need W-9 forms and 1099 documentation, but once properly recorded, they become fully deductible.

Professional fees for accountants, attorneys, and consultants count as ordinary and necessary business expenses. Insurance premiums-general liability, commercial auto, workers’ compensation-reduce taxable income directly. Training, certifications, and industry publications that keep your crew current are legitimate deductions contractors overlook.

The real problem isn’t that these deductions don’t exist; it’s that most contractors don’t track them consistently throughout the year. You find receipts in December, estimate mileage from memory, and guess at home office percentages. That reactive approach costs you thousands.

Start now by implementing a system to capture these expenses as they happen. Construction accounting software tracks equipment purchases, mileage, and project expenses automatically, eliminating guesswork and ensuring nothing falls through the cracks come tax season. With proper tracking in place, you move from leaving money on the table to controlling exactly what hits your bottom line-which sets you up perfectly for the next critical step: timing when that income and those expenses actually count.

The timing of when income and expenses hit your tax return determines how much you owe in any given year. Most contractors treat this as something their accountant handles in December, but that’s far too late. The real money moves happen months earlier through deliberate decisions about accounting methods and expense timing.

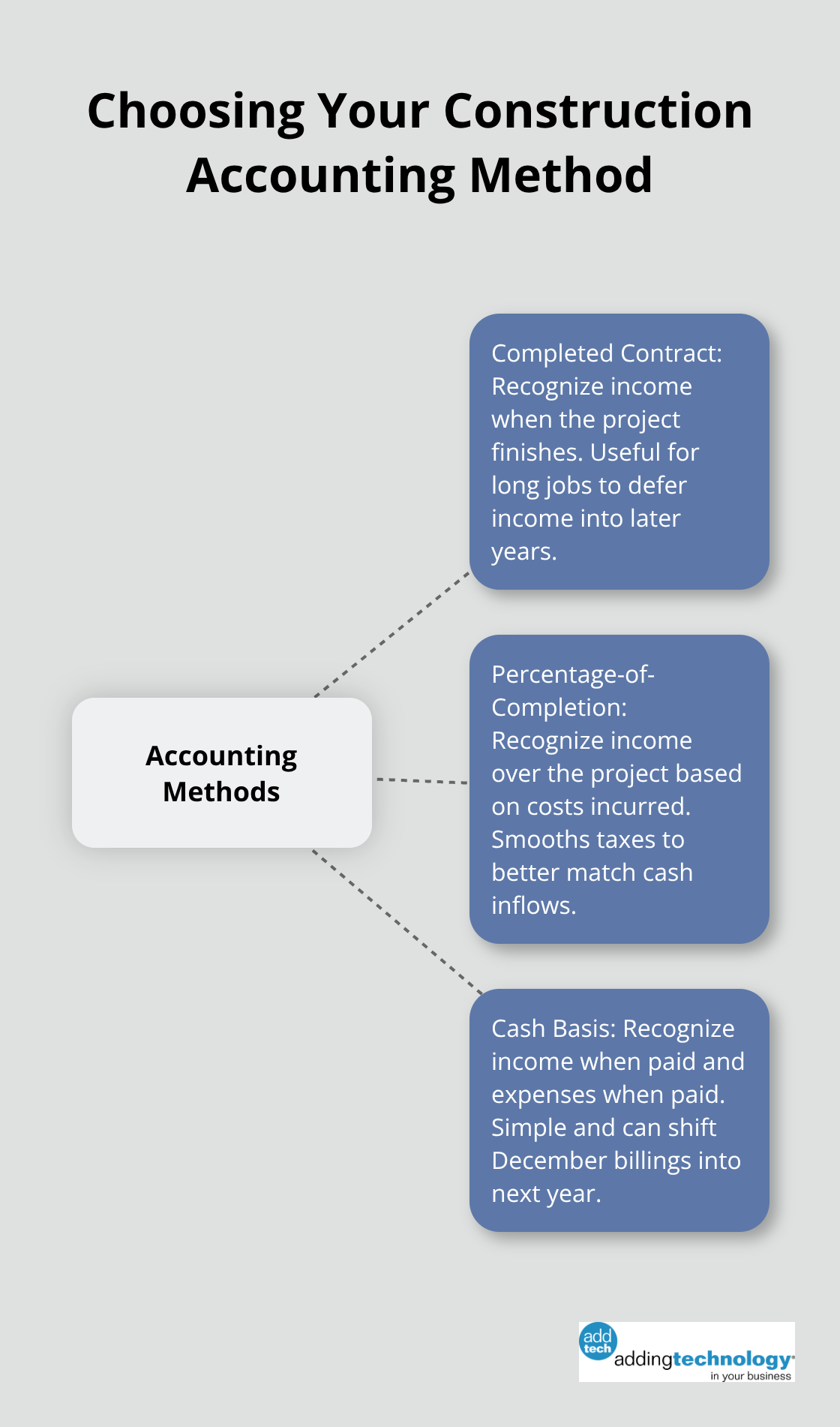

Construction accounting methods exist specifically because project work doesn’t fit standard business patterns. The completed contract method defers income recognition until a project finishes, which means a two-year job generating $500,000 in revenue doesn’t trigger tax liability until completion. This creates significant breathing room for cash flow, especially when multiple projects finish in different years. However, if three major contracts finish in the same December, you’ll face a sudden spike in taxable income that wipes out the deferral benefit.

The percentage-of-completion method spreads income recognition across the project timeline based on costs incurred, aligning taxes more evenly with actual cash inflows. Cash-basis accounting recognizes income only when clients pay you, not when you invoice them, which means delaying invoicing until January 2027 for December 2026 work pushes that revenue into the next tax year entirely. The key is understanding which method fits your project mix and cash flow patterns, then executing it consistently.

Expense timing matters just as much as income recognition. Paying subcontractors before year-end generates deductions in the current year, even if the work spans into January. Year-end equipment purchases placed in service by December 31 qualify for full bonus depreciation deductions immediately rather than waiting for depreciation schedules. Bad debt write-offs for uncollectible accounts receivable must happen before year-end if you’re on an accrual basis to claim them.

Many contractors let retainage sit unpaid from clients, then wonder why their tax bill is higher than expected. Properly timing when you recognize retainage as income-either when billed or when actually received-prevents this surprise. These decisions compound across multiple projects, turning months of planning into thousands of dollars in tax savings.

Starting your tax projection by early November using September 30 financial data gives you time to make meaningful adjustments before December closes. Waiting until late December leaves you scrambling and unable to execute any timing strategies. WIP reports track costs, revenue, and cash flow for every job, giving you actual numbers to work with instead of estimates. That visibility transforms tax planning from guesswork into precision, and it positions you to make the structural decisions that truly move the needle on your bottom line.

The entity you choose for your construction business determines how much tax you actually owe, and most contractors never revisit this decision after formation. An S-corp treats income differently than a sole proprietorship, which treats it differently than an LLC taxed as a partnership. The difference between structures can mean $15,000 to $40,000 annually in tax savings or costs, yet contractors often let this decision sit unchanged for years. Contractors frequently discover this reality only when their accountant mentions it casually during tax season, at which point it’s too late to implement changes for that year.

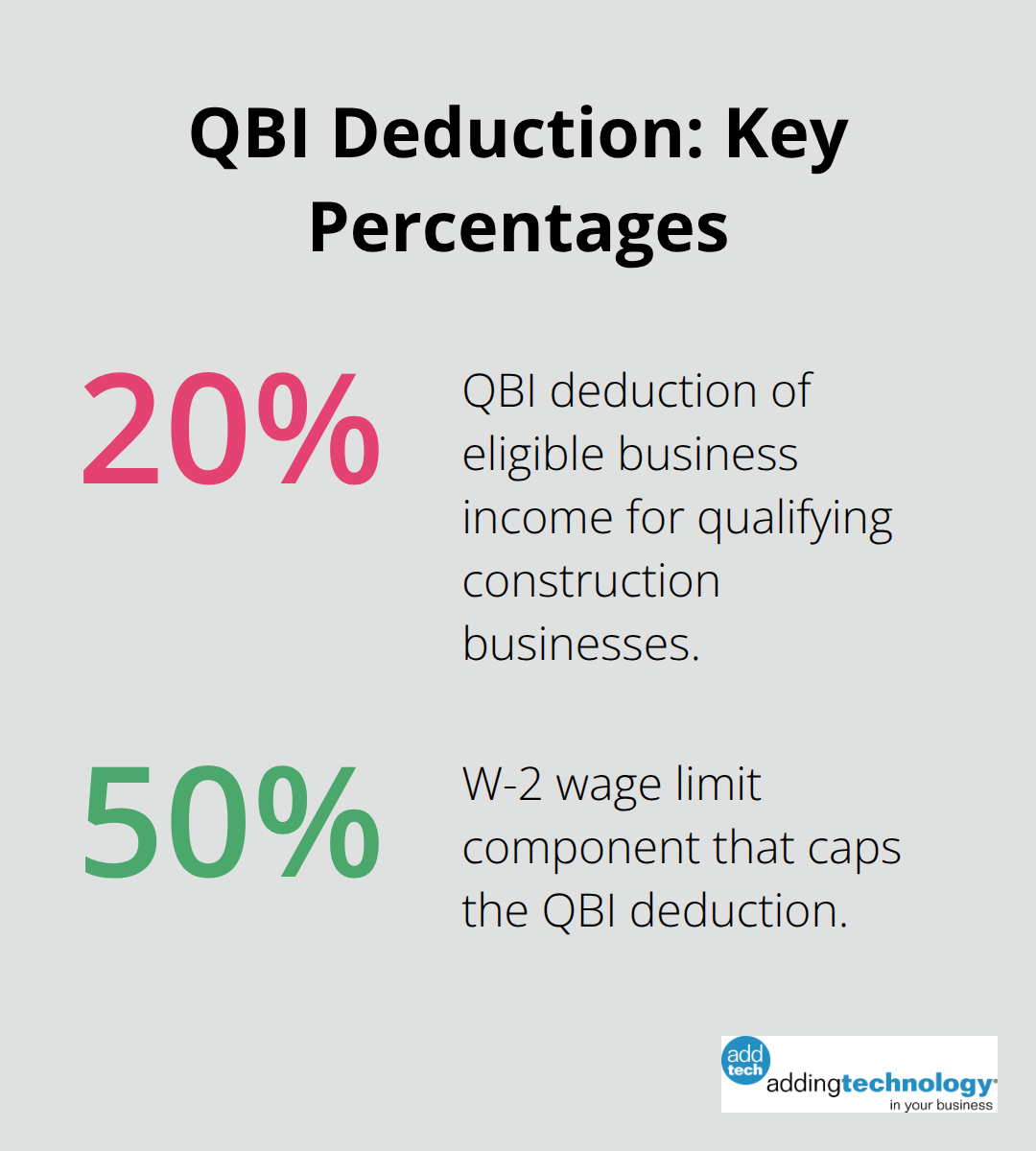

Your business structure interacts directly with the qualified business income deduction, which allows up to 20% of eligible business income for construction businesses but limits the deduction to 50% of W-2 wages paid. A contractor paying $200,000 in W-2 wages can deduct up to $100,000 of W-2 wages toward the QBI calculation, which fundamentally changes how much of your income gets protected from taxation. Pass-through entities like S-corps and partnerships also face state-level pass-through entity tax elections in certain states.

New York offers the NY PTET, allowing the entity itself to pay state taxes at a flat rate, which then becomes deductible federally and avoids the $10,000 SALT cap that hammers individual shareholder deductions. This structure shift alone saves contractors thousands when state taxes are significant.

Misclassifying workers as independent contractors instead of employees creates immediate tax problems and ongoing compliance nightmares. A contractor paying subcontractors $300,000 annually must issue 1099 forms and maintain W-9 documentation, but an employee earning the same amount generates different tax treatment entirely. The contractor classification works when the worker controls how, when, and where the work happens. If you direct daily tasks, provide tools, and control the work schedule, that person should be an employee on payroll. The IRS looks at behavioral control, financial control, and the relationship type when auditing these classifications, and construction is a frequent audit target.

Employees cost more upfront because you pay payroll taxes, workers’ compensation insurance, and potentially benefits. However, the QBI wage limitation works in your favor when you have employees. A contractor with $500,000 in business income but no W-2 wages gets a much smaller QBI deduction than a contractor with the same income who pays $250,000 in W-2 wages. The wage-based limit actually incentivizes hiring, which counteracts the payroll expense argument many contractors use to justify independent contractor relationships. Year-end employee bonuses also maximize the QBI deduction while supporting staff, turning a tax strategy into actual business investment.

Retirement contributions reduce your current taxable income dollar-for-dollar while building wealth for your future. A 401(k) allows up to $23,000 in contributions for 2026, or $30,500 if you’re age 50 or older. A SEP IRA lets you contribute up to 25% of your compensation or $69,000, whichever is less, making it ideal for high-income contractors. A SIMPLE IRA caps contributions at $16,000 annually, or $19,500 if age 50 or older, but requires employer matching contributions. For contractors with few employees or family members in the business, a cash balance pension plan becomes particularly powerful. These plans allow contributions in the $100,000 range annually for older business owners, deferring substantial income while creating a genuine retirement vehicle.

The math is straightforward: a contractor in the 24% federal tax bracket plus 5% state tax saves 29 cents on every dollar contributed to retirement plans. A contractor who contributes $50,000 to a SEP IRA saves roughly $14,500 in combined federal and state taxes. That’s immediate, concrete savings that also protects your future. Many contractors ignore retirement planning until their fifties, then scramble to catch up. Starting at 40 with consistent contributions builds retirement security without the tax desperation that comes later. These contributions must be made by your tax filing deadline, so planning and funding them before year-end ensures you actually capture the deduction in the current tax year.

Construction tax planning works best when you treat it as a year-round discipline rather than a December scramble with your accountant. The strategies we’ve covered-accelerated depreciation, strategic income timing, entity structure optimization, and retirement contributions-compound together to create a tax-efficient operation that protects your cash flow and bottom line. Contractors who win financially aren’t smarter than you; they simply execute these decisions intentionally throughout the year instead of letting them happen by accident.

You track equipment purchases so you don’t miss bonus depreciation deadlines, understand your accounting method and execute it consistently, and review your business structure periodically instead of assuming your original choice still makes sense. Construction accounting is specialized work that requires professionals who understand how project-based revenue creates unique timing challenges that standard business accounting misses entirely. A construction-focused accountant catches opportunities that a general accountant overlooks, and that difference translates directly into thousands of dollars staying in your business.

At adding technology, we help contractors build financial foundations that support real growth through streamlined accounting systems and real-time job costing visibility. When you know your numbers throughout the year, you make better decisions about equipment purchases, expense timing, and business structure. Start now by implementing one change-better equipment tracking, earlier tax projections, or a conversation with a construction-focused professional-and let adding technology help you turn construction tax planning into a competitive advantage.

At adding technology, we know you want to focus on what you do best as a contractor. In order to do that, you need a proactive back office crew who has financial expertise in your industry.

The problem is that managing and understanding key financial compliance details for your business is a distraction when you want to spend your time focused on building your business (and our collective future).

We understand that there is an art to what contractors do, and financial worries can disrupt the creative process and quality of work. We know that many contractors struggle with messy books, lack of realtime financial visibility, and the stress of compliance issues. These challenges can lead to frustration, overwhelm, and fear that distracts from their core business.

That's where we come in. We're not just accountants; we're part of your crew. We renovate your books, implement cutting-edge technology, and provide you with the real-time job costing and financial insights you need to make informed decisions. Our services are designed to give you peace of mind, allowing you to focus on what you do best - creating and building.

Here’s how we do it:

Schedule a conversation today, and in the meantime, download the Contractor’s Blueprint for Financial Success: A Step by-Step Guide to Maximizing Profits in Construction.” So you can stop worrying about accounting, technology, and compliance details and be free to hammer out success in the field.