How Contractors Can Improve Cash Flow Between Construction Projects

Improve cash flow between projects with practical strategies contractors can implement immediately to strengthen finances and reduce cash gaps.

At adding technology, we understand the unique challenges of accounting in construction businesses. The complex nature of project-based work demands specialized financial management practices.

In this blog post, we’ll explore the best practices for construction accounting, from job costing to leveraging cutting-edge software solutions. We’ll provide practical tips to help you streamline your financial processes and boost your bottom line.

Construction accounting differs significantly from standard business accounting. The project-based nature of construction work creates distinct financial challenges since the majority of work is decentralized and tied up in multiple individual projects.

In construction, each project functions as its own mini-business. This requires tracking costs, revenues, and profits for individual jobs rather than overall company performance. It’s a level of detail many other industries don’t require.

A typical construction project involves multiple subcontractors, varying material costs, and long timelines. Each of these elements needs separate accounting, making the process more complex than traditional accounting methods.

Construction projects often span months or years. This long-term nature affects how companies recognize and report revenue. The American Institute of CPAs (AICPA) provides guidance on two main methods for revenue recognition in long-term contracts:

The percentage-of-completion method allows companies to recognize revenue as work progresses. This provides a more accurate picture of a company’s financial health over time. However, it requires careful estimation and tracking of project completion stages.

Construction businesses need to produce and interpret specialized financial statements. The Work-in-Progress (WIP) report stands out as a prime example. This document provides a snapshot of all ongoing projects, showing their financial status at a given point in time.

A WIP report typically includes information such as:

Accurate preparation and understanding of these reports prove essential for making informed decisions about resource allocation and project management.

Cash flow management presents particular difficulties in construction. Managing cash flow is one of the biggest challenges for construction businesses, as large upfront costs for materials and labor often precede payment, which may tie to project milestones or completion.

One common practice in the industry is retainage, where a portion of the payment (typically 5-10%) remains held back until project completion. While this protects clients, it can strain a contractor’s cash flow.

Construction accounting must navigate a complex web of regulations and compliance requirements. These can vary by project type, location, and funding source. For instance, government contracts often require adherence to specific accounting standards and reporting requirements.

Prevailing wage laws, which mandate specific pay rates for workers on public projects, add another layer of complexity to payroll and job costing processes.

Understanding these unique aspects of construction accounting helps businesses better manage their finances and set themselves up for success. Adding Technology specializes in navigating these complexities, ensuring clients have the financial clarity they need to thrive in the competitive construction industry.

The next chapter will explore how to implement effective job costing systems, a critical component of successful construction accounting.

Job costing forms the backbone of successful construction accounting. Let’s explore the essentials of implementing an effective job costing system.

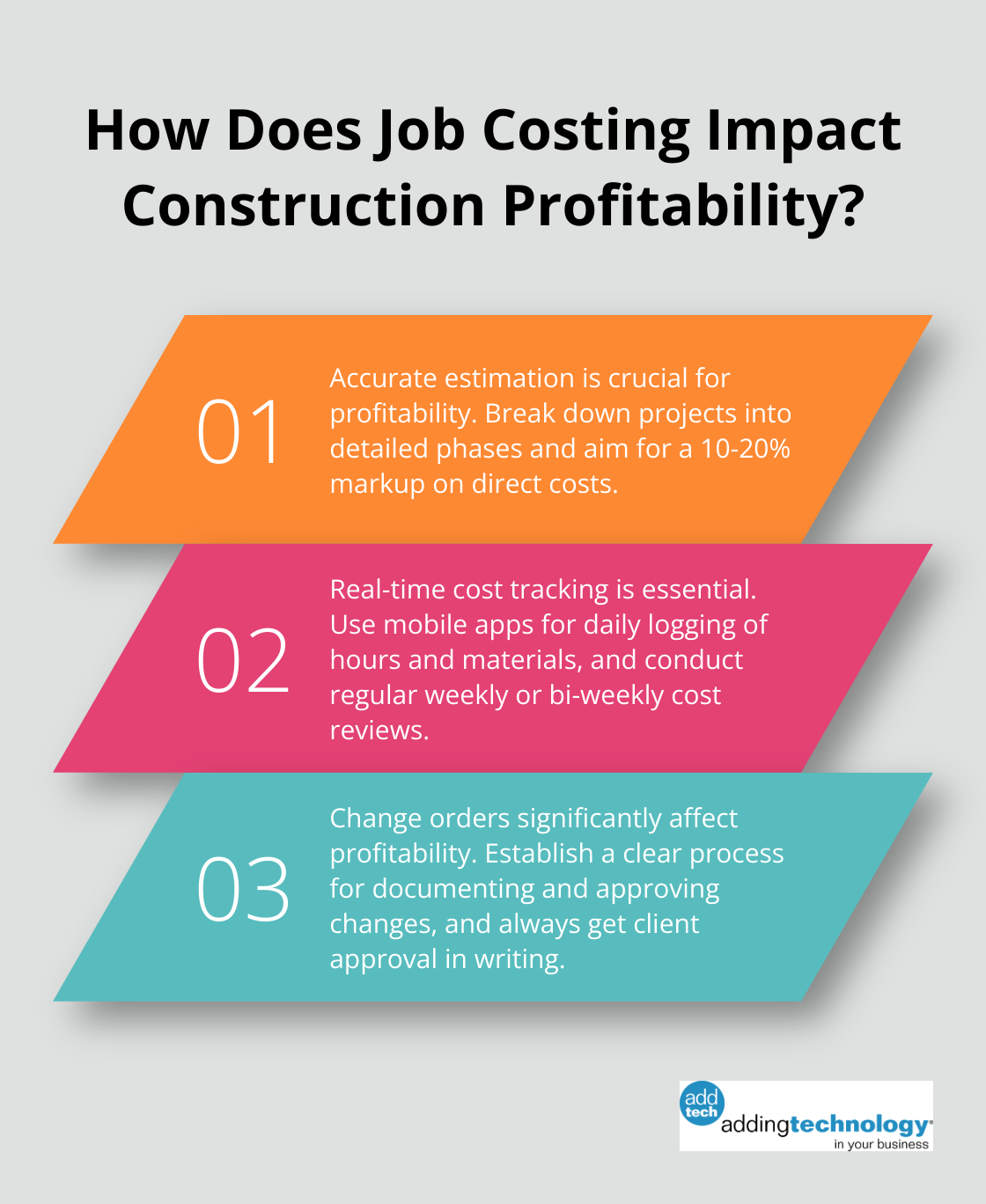

Accurate project estimation determines profitability. Break down each project into detailed phases and tasks. Use historical data from similar projects to inform your estimates. Industry benchmarks can provide valuable insights.

For labor costs, consider hourly rates, productivity levels, and potential overtime. Material costs should include purchase price, delivery fees, and potential waste. Account for equipment costs, whether owned or rented.

Many construction firms underestimate overhead costs. Include a fair allocation of office expenses, insurance, and management salaries in your estimates. Try to achieve a 10-20% markup on direct costs to cover overhead and profit.

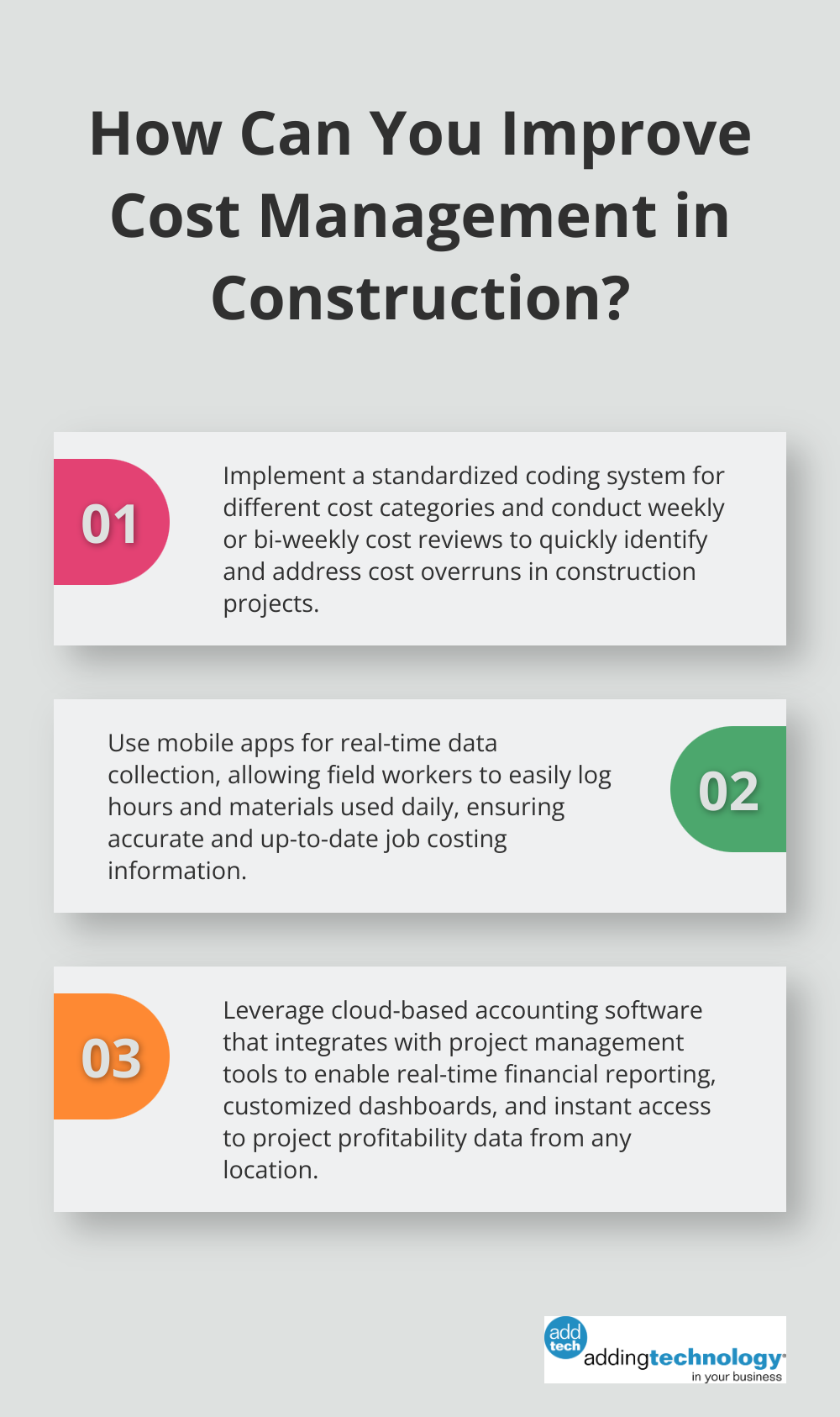

Once a project starts, track actual costs against estimates. Implement a system where field workers can easily log hours and materials used daily. Mobile apps can streamline this process, allowing for real-time data collection.

Create a standardized coding system for different cost categories. This makes it easier to analyze where money is spent and identify any cost overruns quickly. Regular weekly or bi-weekly cost reviews can help catch issues early.

Don’t neglect indirect costs (such as project management time, quality control inspections, and travel expenses). Allocate these costs fairly across projects to get a true picture of profitability.

Change orders can significantly impact project profitability if not managed correctly. Establish a clear process for documenting and approving change orders. This should include a detailed description of the changes, cost implications, and impact on the project timeline.

Price change orders carefully, considering not just the direct costs of materials and labor but also the potential ripple effects on other aspects of the project. Always get client approval in writing before proceeding with changes.

Update your job cost reports regularly to reflect approved change orders. This ensures that your financial projections remain accurate throughout the project lifecycle.

Modern construction accounting software can revolutionize job costing practices. These tools often integrate with project management software, providing real-time financial insights. This level of detail allows for proactive decision-making, helping you stay on budget and on schedule.

Look for software that offers features like:

Adding Technology stands out as a top choice among providers of such specialized construction accounting solutions. Their expertise in the construction industry ensures that their software meets the unique needs of contractors and construction firms.

Effective job costing transforms from a necessary task into a powerful tool for business growth. The next chapter will explore how to leverage technology further in construction accounting, building on the foundation of solid job costing practices.

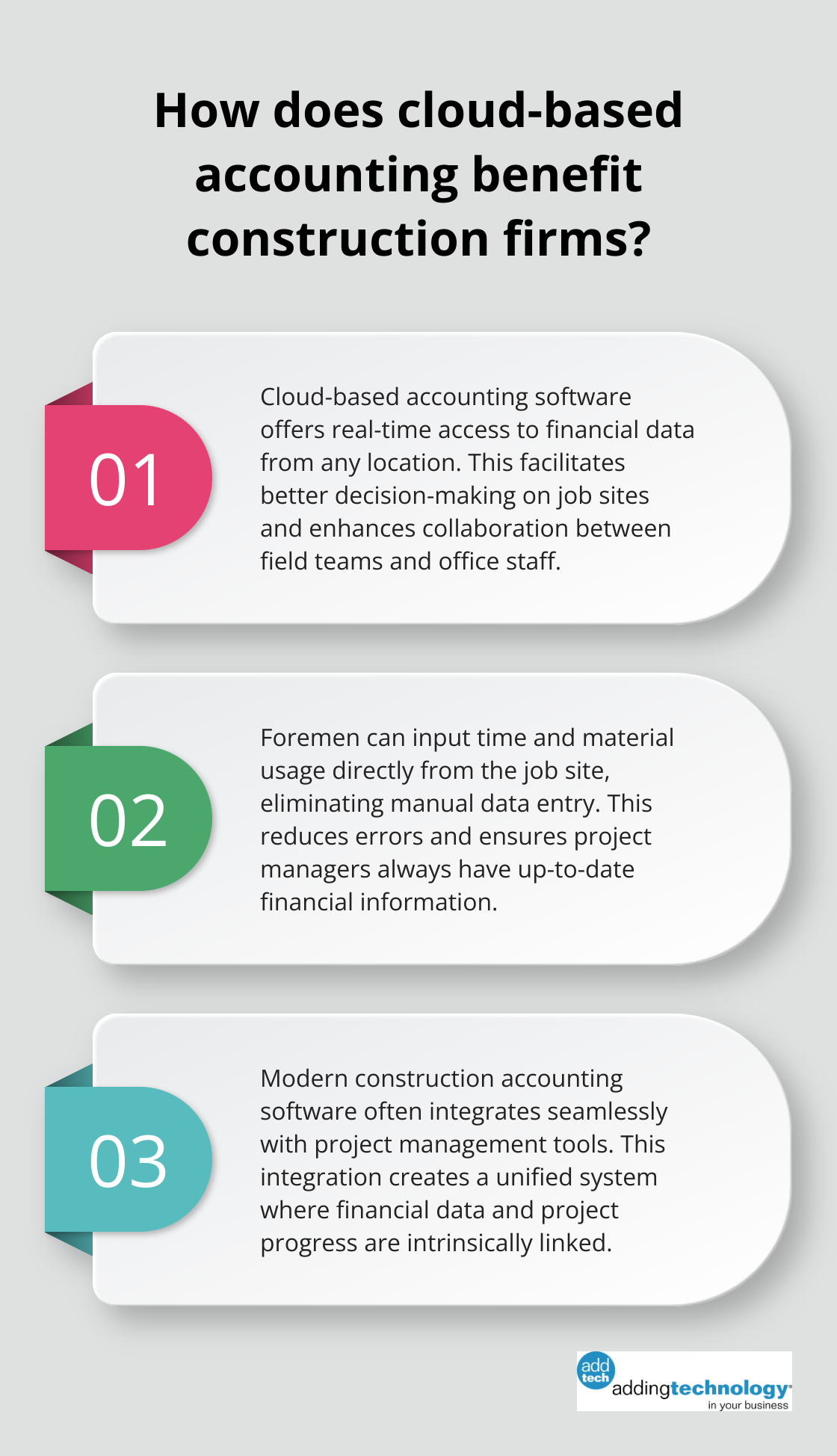

Cloud-based accounting software offers numerous advantages for construction firms. Moving data, applications and platforms to the cloud can create substantial operational and business benefits. This significant uptick in the volume and variety of cloud-based solutions allows real-time access to financial data from any location, which facilitates better decision-making on job sites.

Cloud solutions enhance collaboration between field teams and office staff. Foremen can input time and material usage directly from the job site, which eliminates the need for manual data entry and reduces errors. This real-time data flow ensures that project managers always have up-to-date financial information at their fingertips.

Modern construction accounting software often integrates seamlessly with project management tools. This integration creates a unified system where financial data and project progress link intrinsically. As a result, project managers can make informed decisions based on real-time financial data, while accountants gain insights into project timelines and milestones.

For example, when a project management system approves a change order, it automatically updates the financial projections in the accounting software. This level of integration helps prevent miscommunications and ensures that all team members work with the most current information.

One of the most significant advantages of modern construction accounting technology is the ability to generate real-time financial reports. These reports provide instant insights into project profitability, cash flow, and overall financial health. This method gives contractors a better understanding of whether or not their projects will be profitable before the project is completed.

Advanced reporting features allow construction firms to create customized dashboards that highlight key performance indicators (KPIs) specific to their business needs. For instance, a dashboard might display current job costs against estimates, upcoming payment milestones, and projected cash flow for the next 30 days.

Real-time analysis capabilities enable proactive financial management. If a project starts to go over budget, managers can identify the issue immediately and take corrective action. This level of financial agility can mean the difference between a profitable project and a loss.

While many software providers offer construction accounting solutions, Adding Technology stands out as a top choice. Their specialized focus on the construction industry ensures that their software addresses the unique challenges faced by contractors and construction firms.

Construction businesses should consider the following factors when selecting accounting technology:

Technology adoption in construction accounting is no longer optional-it’s a necessity for staying competitive in today’s fast-paced construction environment. Advanced tools streamline financial processes, improve accuracy, and provide the insights needed to drive profitability and growth.

Accounting in construction businesses requires specialized knowledge and tools to address unique challenges. Accurate job costing and real-time financial visibility enable construction firms to ensure profitability and make informed decisions throughout project lifecycles. Technology has revolutionized construction accounting, with cloud-based solutions and integrated project management tools transforming financial management practices.

We anticipate further technological innovations in construction accounting, including AI-enhanced predictive analytics and blockchain-powered contract management. These advancements will likely improve cost estimations, risk assessments, and payment processes in the construction industry. Construction businesses can optimize their financial management by partnering with industry experts who offer tailored solutions.

Adding Technology provides specialized accounting and financial management services for the construction industry. Their expertise in integrating advanced technology solutions with construction-specific accounting practices helps businesses build a solid financial foundation. As the construction industry evolves, companies that embrace these advancements and implement robust accounting practices will position themselves for long-term success.

At adding technology, we know you want to focus on what you do best as a contractor. In order to do that, you need a proactive back office crew who has financial expertise in your industry.

The problem is that managing and understanding key financial compliance details for your business is a distraction when you want to spend your time focused on building your business (and our collective future).

We understand that there is an art to what contractors do, and financial worries can disrupt the creative process and quality of work. We know that many contractors struggle with messy books, lack of realtime financial visibility, and the stress of compliance issues. These challenges can lead to frustration, overwhelm, and fear that distracts from their core business.

That's where we come in. We're not just accountants; we're part of your crew. We renovate your books, implement cutting-edge technology, and provide you with the real-time job costing and financial insights you need to make informed decisions. Our services are designed to give you peace of mind, allowing you to focus on what you do best - creating and building.

Here’s how we do it:

Schedule a conversation today, and in the meantime, download the Contractor’s Blueprint for Financial Success: A Step by-Step Guide to Maximizing Profits in Construction.” So you can stop worrying about accounting, technology, and compliance details and be free to hammer out success in the field.