Construction Compliance Checklist: Staying Auditable On Every Job

Track construction compliance requirements with our essential checklist to keep every job auditable and protect your business.

Most contractors either ignore overhead or dump it all on one project, killing profitability on others. We at adding technology have seen this destroy margins on jobs that looked profitable on paper.

Overhead allocation methods aren’t accounting busywork-they’re the difference between knowing which projects actually made money and guessing. When you allocate shared costs fairly across jobs, you can finally see your true project profitability and price future work correctly.

Overhead in construction isn’t just office rent and insurance. Most contractors underestimate what belongs in this category, which means their overhead rates are wrong from the start. A contractor thinks overhead is 8% when it’s actually 15%, and suddenly bids that looked solid are underwater. Overhead includes anything your company spends money on that isn’t directly tied to a specific project.

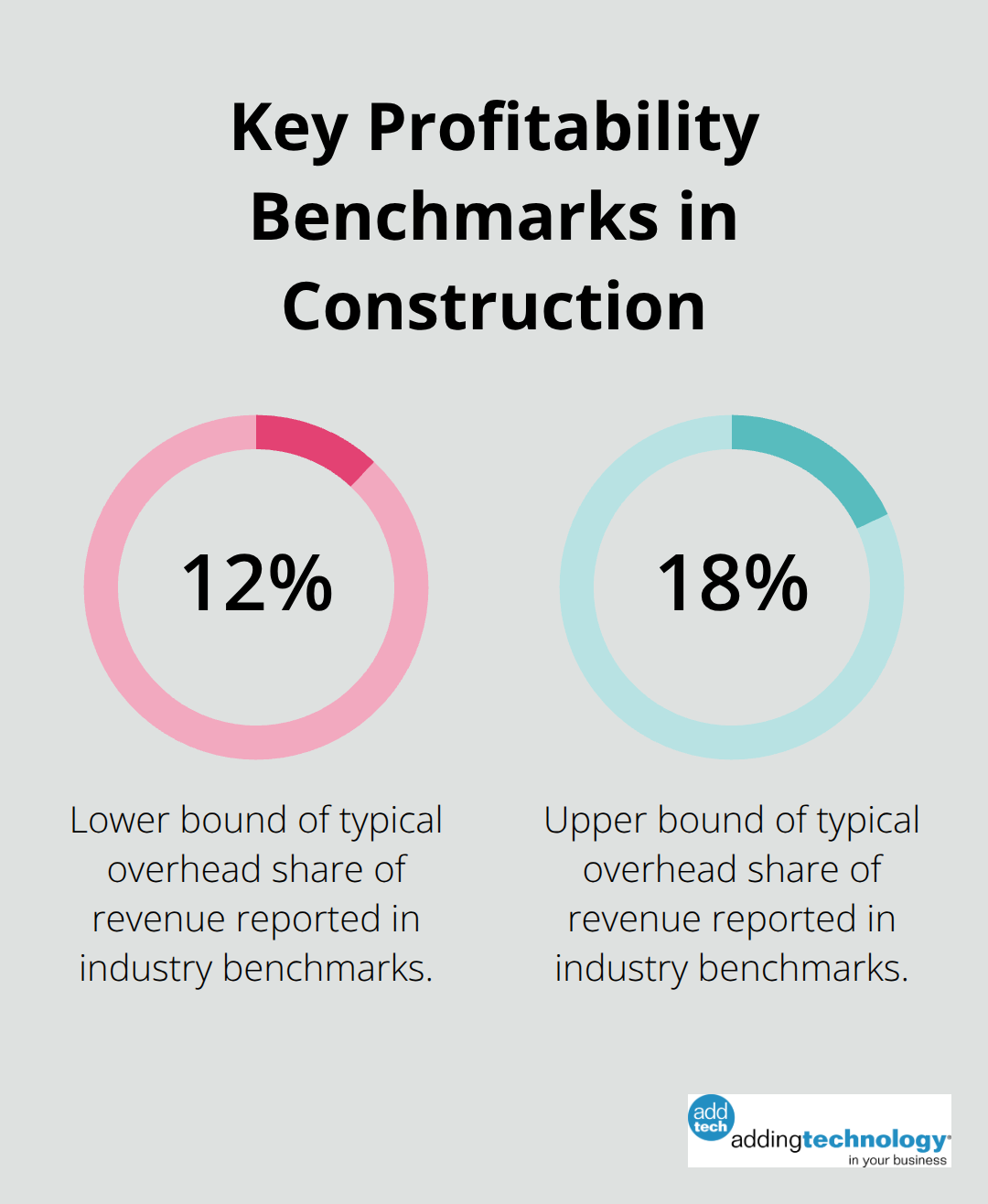

This covers depreciation on equipment and vehicles, fuel for the job site shuttle, indirect labor like project managers and safety officers who move between jobs, general liability and workers’ compensation insurance, office supplies, utilities, accounting software subscriptions, license and permit fees, legal services, and marketing. The CFMA’s 2024 Financial Benchmarker found that Best in Class construction firms achieve 11.9% pre-tax net income-and superior overhead management is a major reason why.

Many contractors miss that overhead splits into fixed and variable costs. Fixed overhead stays constant month to month regardless of project volume: rent typically runs $2,000 to $5,000 monthly depending on office size, and insurance premiums cover administrative staff salaries. Variable overhead fluctuates with your workload: utilities spike when you run multiple job sites, and temporary equipment rentals increase during busy seasons. If you don’t separate these, you can’t forecast accurately or adjust when project volume drops.

When you lump all overhead into one project or apply the same rate across different job types, you’re essentially guessing at profitability. A small residential renovation absorbs overhead meant for a six-month commercial build, making it look unprofitable when it actually was. A labor-intensive project gets charged the same overhead rate as a material-heavy one, even though they demand different levels of project management.

Fair allocation changes this picture. When you allocate overhead proportionally to how each project actually consumes shared resources, you finally see which work truly makes money. Contractors who implement proper allocation methods report clearer visibility into which job types are actually profitable and can adjust pricing on future bids accordingly. The result is pricing that recovers your actual costs instead of leaving money on the table or overcharging clients.

Overhead and markup directly impact your profit margin. Without visibility into how overhead actually flows across your projects, you’re flying blind on half the equation. This is where the right allocation method becomes your competitive advantage-and why choosing the approach that fits your operation matters so much.

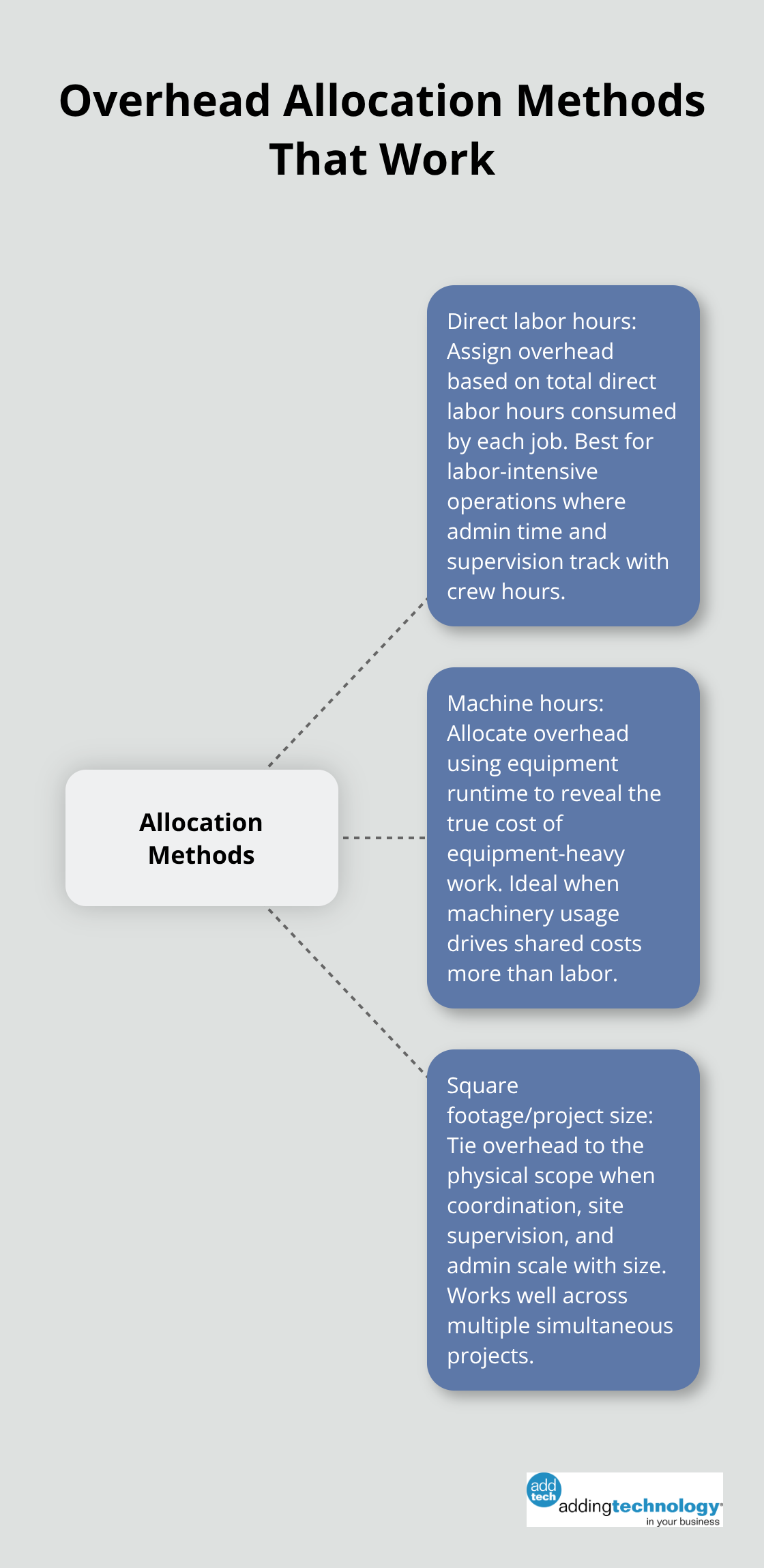

The direct labor hour method dominates construction because it’s simple: you divide total overhead by total direct labor hours worked across all projects, then assign overhead to each job based on how many hours it consumed. If your annual overhead is $240,000 and your crews logged 12,000 direct labor hours last year, your overhead rate is $20 per hour. A residential project that used 400 labor hours receives $8,000 in overhead allocation. This method works well for labor-intensive contractors where project managers, safety officers, and equipment operators move between jobs in proportion to labor activity. The weakness appears fast: a project that’s material-heavy or equipment-dependent but light on labor gets undercharged, while a labor-intensive job absorbs overhead it didn’t cause.

The direct labor hour method makes sense if your overhead genuinely tracks with labor volume. A framing crew, concrete contractor, or carpentry-focused operation typically finds this approach accurate because administrative time, project management, and equipment depreciation do scale with crew size and hours on site. Track your labor hours carefully through timesheets or job tracking software, and this method becomes reliable. The trap is assuming it works for all overhead categories equally. Equipment depreciation might not correlate with labor hours if you own heavy machinery that sits idle between jobs. Insurance costs don’t change based on whether a project runs 100 or 500 labor hours. Most contractors benefit from applying the direct labor hour method to labor-related overhead only-administrative salaries, payroll taxes, safety officer time-and handling equipment and facility costs separately.

The machine hour method allocates overhead based on equipment runtime rather than labor. A contractor running an asphalt paving operation, concrete cutting service, or heavy equipment fleet tracks machine hours instead of labor hours. If a compressor runs 40 hours on one project and 60 hours on another, overhead allocation follows that ratio. This method reveals the true cost of equipment-intensive work that might employ few workers but consume significant machinery. Equipment-heavy operations can’t use labor hours as their primary driver without distorting costs. The challenge surfaces when you own equipment that sits idle or shared equipment that moves between multiple concurrent projects. You’ll need accurate equipment logs-maintenance records, fuel consumption, or runtime meters-to make this method work. Most contractors find they need both labor and machine hour tracking rather than choosing one exclusively.

Square footage or project size allocation works when overhead consumption correlates with the physical scope of work. A general contractor managing a 5,000-square-foot renovation allocates less overhead than a 50,000-square-foot commercial build because the larger project requires more site supervision, coordination, and administrative oversight. This method works particularly well for firms doing multiple projects simultaneously where project management costs, site office expenses, and coordination time scale visibly with project size. The advantage is simplicity: you measure the scope once at the bid stage and use that figure consistently. The disadvantage is that square footage alone misses complexity. A 10,000-square-foot historic renovation with specialty requirements demands far more project management than a 10,000-square-foot straightforward warehouse shell. Two projects of identical size can consume vastly different overhead if one involves multiple trades, change orders, and tight coordination while the other runs smoothly with minimal surprises.

Most contractors who achieve strong overhead allocation don’t rely on a single method. You might allocate labor-related overhead by direct labor hours, equipment costs by machine hours, and facility expenses by project size. This hybrid approach reflects how your actual overhead flows across different projects.

The key is avoiding double allocation-don’t count the same overhead expense twice across different methods. Your accounting software should support this flexibility, allowing you to assign different overhead categories to different allocation bases. Once you understand which method (or combination) matches your operation, the next step is building systems that capture the data you need to make these allocations work.

Your business structure determines which allocation method actually works. A roofing contractor with crews working multiple residential projects simultaneously needs a different approach than a commercial GC managing one large building at a time. The first step is honest assessment: what does your overhead actually follow? If your project managers spend proportionally more time on larger jobs, square footage allocation makes sense. If your crews move between projects and overhead scales with labor volume, direct labor hours become your baseline. A concrete contractor running equipment across multiple sites needs machine hours tracked separately. Most contractors operate as hybrids-some overhead tracks with labor, some with equipment, some with project scope. This matters because the wrong allocation method produces wrong bids, and wrong bids destroy margins faster than anything else.

Pull your general ledger for the last 12 months and categorize every indirect cost. Don’t estimate-use actual numbers. Most contractors find overhead runs 12%–18% of revenue, according to industry data, but yours might be different. Separate fixed costs (rent, salaried staff, insurance premiums) from variable costs (utilities, temporary equipment rental, subcontract supervision). Then track where each cost actually originates. Equipment depreciation correlates with machinery use, not labor hours. Administrative salaries might track with project count, not project size. Safety officer time definitely tracks with labor hours. Once you see this pattern, the allocation method becomes obvious. A roofer with high equipment costs shouldn’t use labor hours alone. A framing contractor with minimal equipment but high crew costs should. Construction accounting software that integrates timesheets, equipment logs, and project data reveals these patterns automatically, saving weeks of manual analysis.

You cannot allocate what you don’t track. If you choose direct labor hours as your primary allocation base, every crew member needs accurate timesheets tied to specific projects. If machine hours matter, equipment needs runtime logs or GPS tracking. If project size drives overhead, jobs must be measured consistently at bid stage. Most contractors underestimate the data work required. You need systems in place before you calculate your first overhead rate. Advanced software solutions eliminate manual spreadsheet tracking and reduce errors dramatically. The software captures labor hours from job site timesheets, integrates equipment usage data, and calculates overhead allocation automatically each month. This prevents the common mistake of allocating based on estimates rather than actual project consumption. Real data beats assumptions every single time. Once your systems run for three to four months, you’ll have enough actual data to calculate accurate overhead rates rather than guessing.

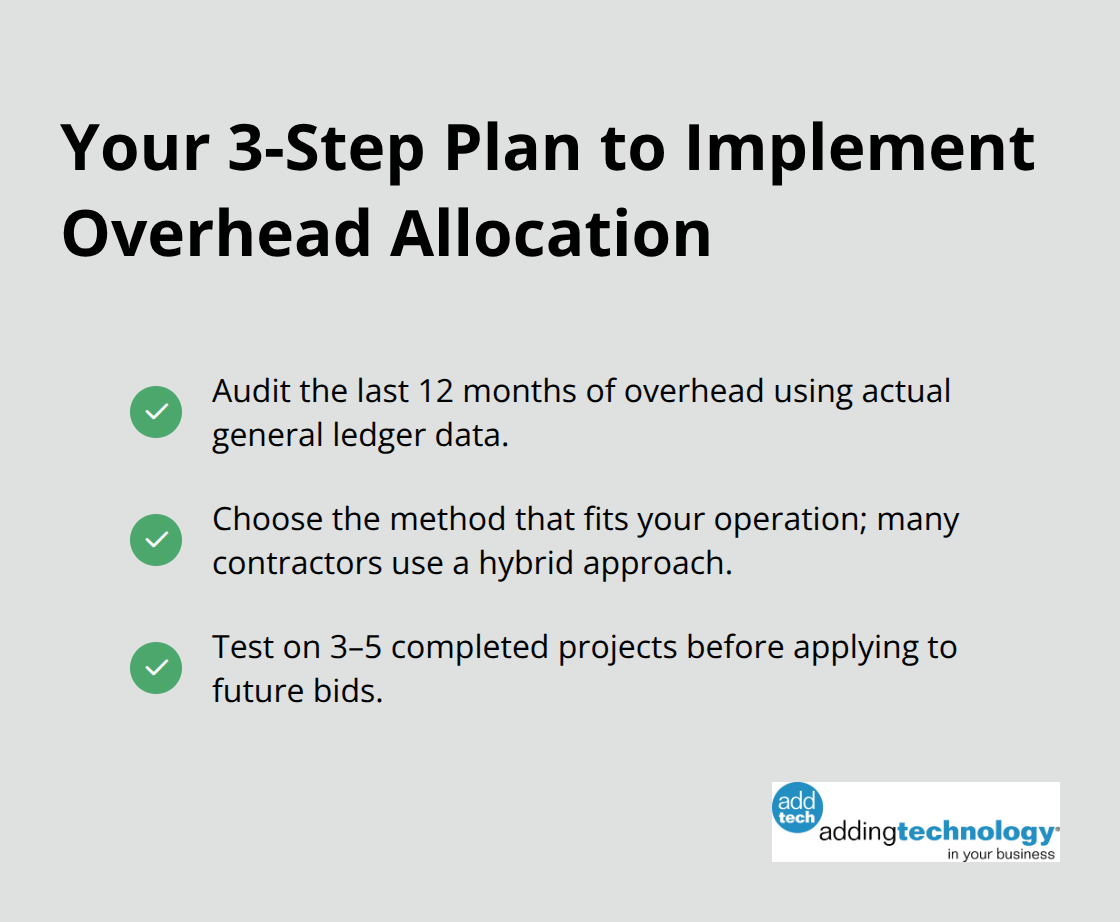

Before applying a new allocation method to future bids, run it backward on three to five completed projects. Calculate what overhead would have been allocated under your chosen method, then compare to what you actually allocated (or didn’t allocate). Did the method produce reasonable results? Would those projects have been priced differently? Most contractors find their first allocation attempt produces surprises-some projects appear far more profitable than they seemed, others less so. This is exactly why you test before committing. If the results look wrong, adjust your allocation basis or shift to a hybrid approach. If results look accurate, you’ve found your method. The test phase typically takes two to three months and costs almost nothing except time. It prevents the expensive mistake of implementing a flawed allocation system across your entire business.

Fair overhead allocation transforms how you see your business. When you stop guessing at profitability and start tracking actual costs across projects, your margins improve immediately. Contractors who implement proper overhead allocation methods report clearer visibility into which work truly makes money and adjust pricing on future bids accordingly. The CFMA’s 2024 Financial Benchmarker shows Best in Class firms achieve 11.9% pre-tax net income, and superior overhead management is a major reason why.

Getting started requires three concrete steps. First, audit your overhead for the last 12 months using actual numbers from your general ledger, not estimates. Second, choose your allocation method based on what you find-most contractors benefit from a hybrid approach that allocates labor-related overhead by direct labor hours, equipment costs by machine hours, and facility expenses by project size. Third, test your chosen method on three to five completed projects before applying it to future bids.

Building a transparent operation starts with systems that capture real data. Timesheets tied to projects, equipment logs, and consistent job measurements provide the foundation for accurate allocation. Construction accounting software eliminates manual spreadsheet tracking and calculates overhead allocation automatically each month, preventing the common mistake of allocating based on estimates rather than actual consumption.

At adding technology, we know you want to focus on what you do best as a contractor. In order to do that, you need a proactive back office crew who has financial expertise in your industry.

The problem is that managing and understanding key financial compliance details for your business is a distraction when you want to spend your time focused on building your business (and our collective future).

We understand that there is an art to what contractors do, and financial worries can disrupt the creative process and quality of work. We know that many contractors struggle with messy books, lack of realtime financial visibility, and the stress of compliance issues. These challenges can lead to frustration, overwhelm, and fear that distracts from their core business.

That's where we come in. We're not just accountants; we're part of your crew. We renovate your books, implement cutting-edge technology, and provide you with the real-time job costing and financial insights you need to make informed decisions. Our services are designed to give you peace of mind, allowing you to focus on what you do best - creating and building.

Here’s how we do it:

Schedule a conversation today, and in the meantime, download the Contractor’s Blueprint for Financial Success: A Step by-Step Guide to Maximizing Profits in Construction.” So you can stop worrying about accounting, technology, and compliance details and be free to hammer out success in the field.