Contractor Licensing Requirements: Navigating Your Regulatory Landscape

Understand contractor licensing requirements and avoid compliance mistakes that cost money.

Construction projects fail when risk management is an afterthought. We at adding technology have seen firsthand how a solid construction risk management plan separates successful projects from costly disasters.

Without proper planning, a single overlooked hazard can derail timelines and budgets. This guide walks you through identifying risks, building defenses, and staying ahead of problems before they happen.

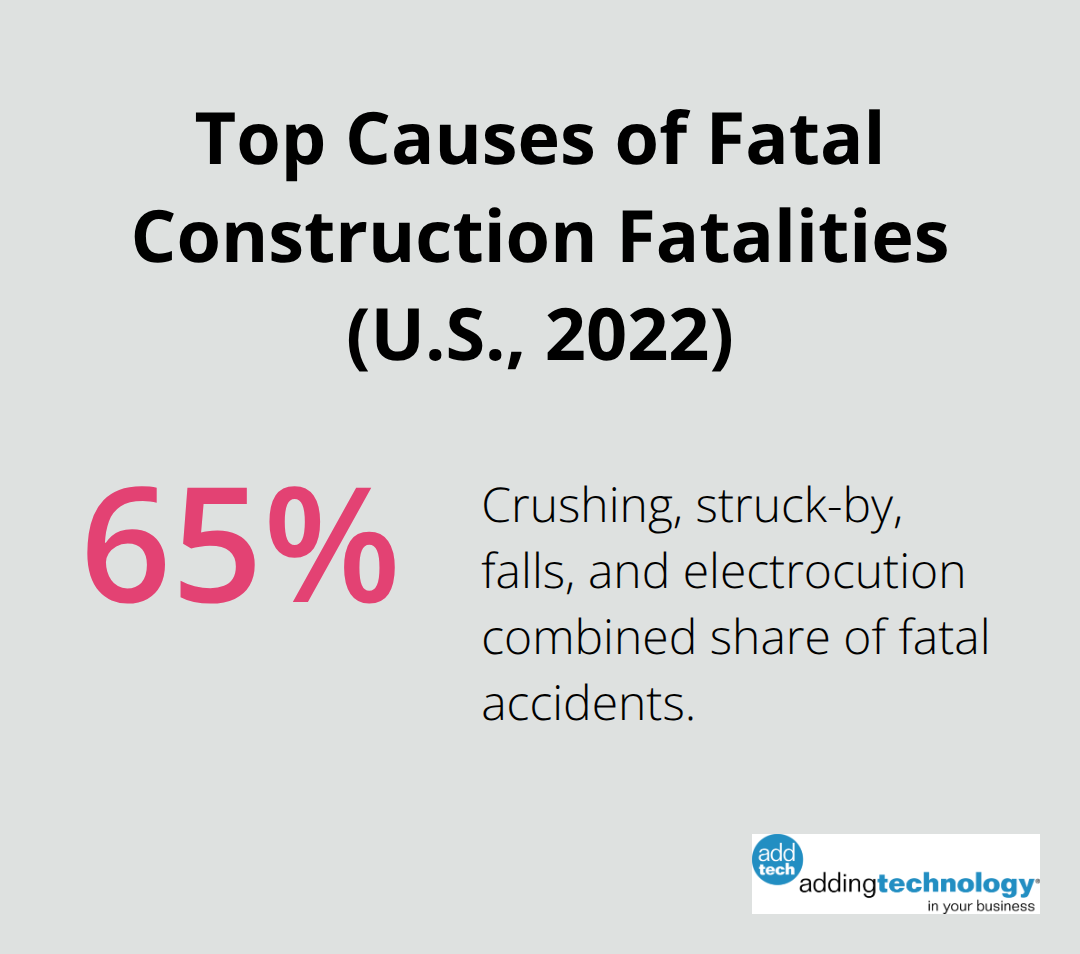

The U.S. construction industry recorded over 1,000 fatal work-related accidents in 2022, with 65% caused by crushing, being struck by objects, falls, and electrocution. These numbers matter because they represent the most common threats on job sites, and they’re preventable. Construction risks fall into five distinct categories: project management, financial, legal, safety, and environmental. Each requires a different response strategy.

Project management risks include delays and poor scheduling, which cost money fast. Financial risks range from material cost fluctuations to budget overruns that spiral without control. Legal risks emerge from contract disputes and labor-law violations. Safety risks are the most visible but often the least well-managed. Environmental risks cover pollution, waste disposal, and regulatory compliance. Most contractors focus heavily on safety while neglecting financial and legal risks, which often cause more project damage overall.

Identifying risks requires structured thinking, not guessing. Gather your project team, including the site superintendent, estimator, and safety manager, and run a risk identification session using concrete examples from your past projects. The Delphi method works well here: ask each team member to list risks independently, then consolidate and discuss them as a group. This prevents groupthink and surfaces issues one person might dismiss.

Document everything in a risk register with specific fields: risk ID, description, category, probability, impact score, owner, and mitigation action. This living document becomes your reference point throughout the project. Include lessons learned from similar past projects, as these patterns repeat across job sites. A practical tip: ask your subcontractors what risks they see. They work on multiple projects and spot patterns you might miss.

Material cost volatility is a current concern. Lock in prices early through fixed-price contracts with suppliers and explore alternative materials that meet specs at lower cost.

Once you’ve identified risks, assess them using both qualitative and quantitative methods. Qualitative assessment uses simple scales: low, medium, or high probability and impact. Quantitative assessment assigns numbers, allowing you to calculate risk scores. Build a probability-impact matrix with probability on one axis (rare to almost certain) and impact on the other (none to catastrophic). Plot each risk on this matrix to see which ones demand immediate attention.

High-probability, high-impact risks get resources first. For example, a material price spike has high probability and high impact; a minor scheduling slip has high probability but low impact. Prioritize accordingly. Document your assessment rationale so stakeholders understand why certain risks matter more. This transparency builds trust and aligns the team.

Real-time expense tracking throughout the project helps you catch financial risks early before they become crises. With visibility into costs as they happen, you spot budget threats before they spiral. This data-driven approach transforms risk management from reactive firefighting into proactive planning. The next step moves beyond identification and assessment-it’s time to build the defenses that actually stop risks from becoming project disasters.

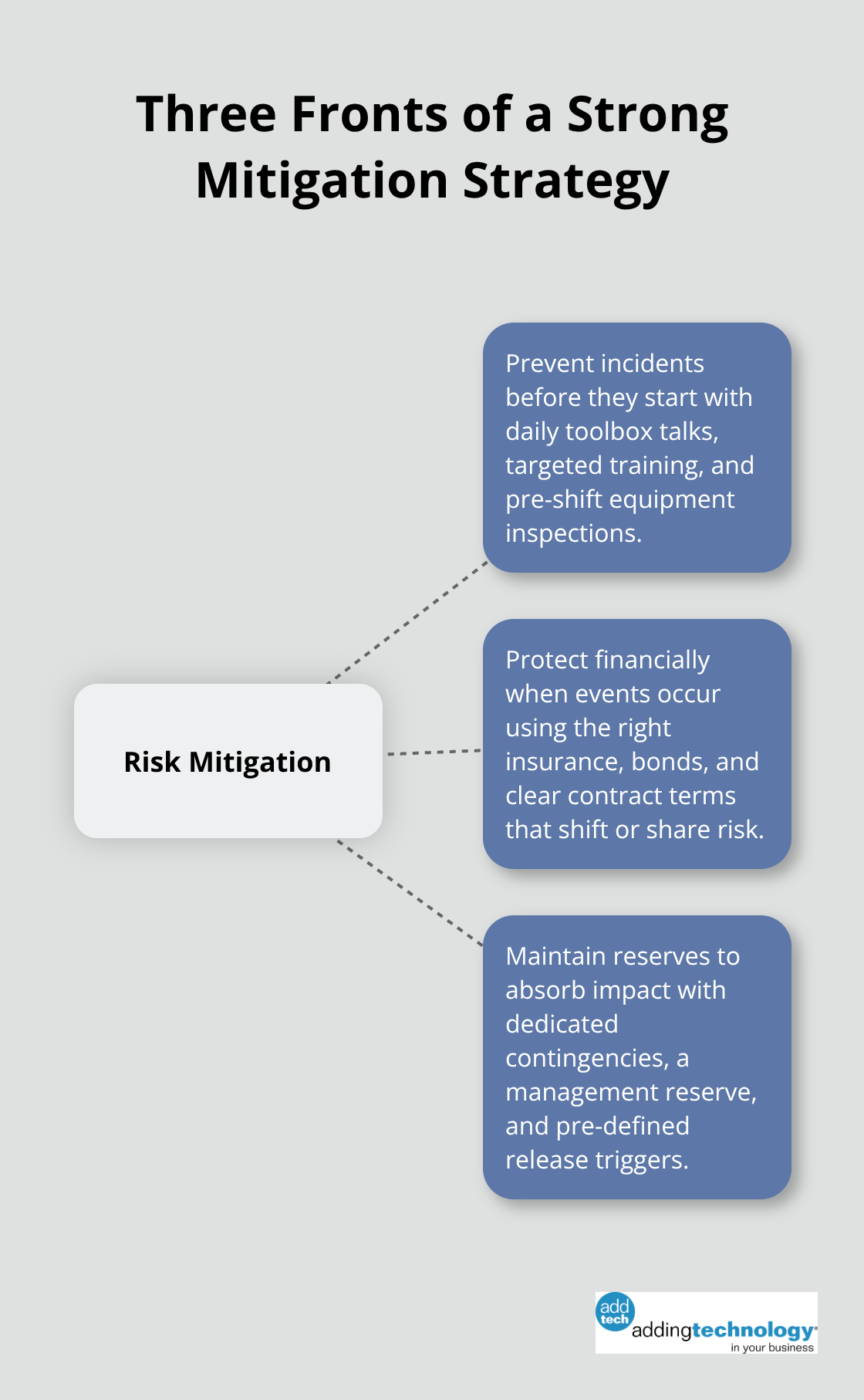

Identifying risks means nothing without action. Contractors who complete thorough risk assessments then fail to implement defenses watch preventable problems destroy project margins. Your mitigation strategy must address three fronts simultaneously: preventing incidents before they start, protecting yourself financially when they occur, and maintaining reserves to absorb the impact.

Prevention beats cleanup every time. On-site safety protocols reduce injuries directly, which means fewer delays and lower workers’ compensation costs. OSHA compliance isn’t optional-it’s the floor. Implement daily toolbox talks focused on the specific hazards your crew faces that day, not generic safety speeches. Assign a dedicated safety manager whose sole job is hazard identification and correction, not someone juggling safety alongside other duties. Equipment inspections happen before work starts, not after failure. A predictive maintenance program catches equipment problems before they strand your crew. Document everything: inspection dates, findings, corrective actions. This documentation protects you legally and creates a pattern showing you took reasonable precautions.

Material price volatility demands early action. Lock in supplier prices through fixed-price contracts before market swings hurt you. Diversify your suppliers so one shortage doesn’t paralyze the project. Alternative materials that meet specifications can replace expensive items without compromising quality. These preventive moves cost less than managing crises.

Insurance alone won’t save you. General liability, workers’ compensation, and equipment coverage are baseline requirements, but they have limits and gaps. Review your coverage annually with an insurance broker who understands construction, not a generalist. Bonds-performance bonds, payment bonds, bid bonds-create a separate layer of protection that insurance doesn’t cover. They guarantee you’ll perform or someone else completes the work at your cost. Understand the difference between what insurance covers and what bonds guarantee; many contractors confuse the two.

Real-time job costing reveals cost overruns before they consume your profit. With visibility into actual costs against budget, you catch financial drift early and adjust spending before problems escalate. Contingency reserves must be separate from your standard budget. Set aside funds specifically for identified risks-material price increases, weather delays, design changes-with clear triggers for when you release that money. A separate management reserve covers unknown unknowns. Most contractors underfund contingencies or use them as profit padding; neither approach works. Calculate contingencies using historical project data from your own jobs, not industry averages. Your risk profile differs from competitors’ profiles.

Contingency plans separate controlled problems from chaos. Identify your top five risks and develop specific response plans for each. If a key subcontractor fails, who replaces them and how quickly? If material delivery delays by six weeks, which activities can shift? If weather shuts down the site, what’s your rescheduling protocol? Test these plans before you need them. Walk through scenarios with your team and adjust based on what you learn.

Assign a risk owner for each major risk-someone accountable for monitoring that risk and executing the response plan when triggered. That person needs authority to make decisions without waiting for approvals. Resource allocation means money, equipment, and personnel. When a risk hits, do you have the budget to respond, or will the response destroy your contingency? Can you access additional equipment quickly if yours fails, or will you wait weeks for replacements? Can key personnel shift to respond to crises, or are they locked into other tasks? These questions must be answered before the project starts, not during an emergency. With your defenses in place, the next critical step is establishing how you’ll track whether those defenses actually work.

A risk management plan sitting in a drawer does nothing. Construction teams that build solid plans then never check whether those plans actually prevent problems watch their defenses fail silently until a crisis hits. Your mitigation strategies collapse without verification, and you realize too late that your approach never worked. Tracking performance means establishing concrete metrics tied to your actual risks, reviewing those metrics regularly with your team, and adjusting your approach when data shows problems. This isn’t about collecting vanity metrics that sound good in reports. Focus on leading indicators that predict problems before they happen, not lagging indicators that confirm damage after the fact. For safety risks, track near-miss reports and hazard observations daily, not injury rates after people get hurt. For financial risks, monitor cost variance weekly against budget, not profit loss after the project ends. For schedule risks, watch task completion rates and long lead time procurement status, not delays announced when the deadline passes. Assign one person ownership of each metric and require them to report findings to the project team every week. Make the data visible on job site dashboards or in your project management system so everyone sees performance trending upward or downward in real time.

Your key performance indicators must connect directly to your identified risks, not generic construction metrics. If material cost volatility ranks as your highest financial risk, track actual material costs against locked-in contract prices weekly and measure price variance as a percentage. If equipment failure threatens your schedule, log equipment downtime hours and compare that against predicted downtime in your risk assessment. If subcontractor performance creates project risk, measure their work completion rates against schedule and defect rates on their deliverables. These specific metrics tell you whether your mitigation strategies work. A contractor locked in material prices to mitigate cost risk, then never tracked whether those locked prices actually held. Three months into the project, suppliers started charging additional fees for expedited delivery that weren’t part of the original contract. The locked price meant nothing because the metric wasn’t measuring the actual cost paid. Once they started tracking total material cost including all fees, they caught the problem and renegotiated terms with suppliers. Your metrics need to measure what actually happens on the job, not what you assumed would happen.

Weekly risk reviews with your core team take 30 minutes and prevent expensive surprises. Gather the project manager, superintendent, estimator, and safety manager every Monday and walk through your risk register. For each high-priority risk, ask three questions: What’s the current status? Has anything changed since last week? Do we need to adjust our response? This consistency prevents risks from sliding off everyone’s radar. Many contractors conduct risk reviews at project kickoff then never mention risks again until something breaks. That’s not a review process, that’s hope. Monthly reviews with broader stakeholders including owners and subcontractors surface risks you missed and build accountability across the team. Quarterly deep-dive reviews examine whether your mitigation actions actually reduced risk levels. If a risk hasn’t decreased after three months of mitigation efforts, your response strategy isn’t working and needs replacement. Document these reviews in writing, even if just email summaries, so you have a record of what changed and why. This documentation becomes invaluable when disputes arise or when you review lessons learned after project completion.

Risk communication fails when information sits in a risk register that only the project manager reads. Translate your risks into language your crew understands. A high-probability weather delay risk becomes a daily toolbox talk about site protection measures and rescheduling protocols. A financial risk around material availability becomes a conversation with subcontractors about what happens if their materials don’t arrive on schedule. A safety risk around fall hazards becomes specific work procedures and equipment checks, not abstract risk statements. Use your project management system or job site dashboard to show risk status visually so people grasp severity without reading detailed reports. Red, yellow, and green status indicators communicate faster than paragraphs. When a risk status changes, notify affected teams immediately, not at the next monthly meeting. If your material supplier signals a price increase, tell your estimator and project manager the same day so they can explore alternatives. If weather forecasts show a storm approaching, alert the team 48 hours before so they can prepare, not the morning of the storm when preparation is impossible. This real-time communication transforms risk management from a planning document into an active operational practice that shapes daily decisions.

A solid construction risk management plan transforms from a static document into an active operational system that shapes decisions from kickoff through closeout. Contractors who treat risk management as core operations rather than compliance overhead build sustainable businesses and report fewer delays, tighter cost control, and lower insurance premiums as their safety records improve. Your team gains confidence when they know risks receive tracking and attention, which reduces stress and strengthens relationships with subcontractors and suppliers who prefer working with contractors that communicate risks clearly and plan responses in advance.

Implementation starts this week, not next month. Pull your team together and conduct a risk identification session using your past projects as reference points, then build your risk register with the five categories, assign owners, and schedule weekly reviews. Calculate contingency reserves based on your actual historical data rather than industry guesses, lock in material prices early, diversify suppliers, implement daily safety protocols with a dedicated owner, and track real-time costs and schedule performance against your baseline.

These actions cost nothing except time and discipline, yet they prevent the expensive surprises that destroy margins and project timelines. Adding Technology specializes in real-time job costing and financial systems built for construction, which gives you the cost visibility your construction risk management plan requires to catch financial risks before they spiral.

At adding technology, we know you want to focus on what you do best as a contractor. In order to do that, you need a proactive back office crew who has financial expertise in your industry.

The problem is that managing and understanding key financial compliance details for your business is a distraction when you want to spend your time focused on building your business (and our collective future).

We understand that there is an art to what contractors do, and financial worries can disrupt the creative process and quality of work. We know that many contractors struggle with messy books, lack of realtime financial visibility, and the stress of compliance issues. These challenges can lead to frustration, overwhelm, and fear that distracts from their core business.

That's where we come in. We're not just accountants; we're part of your crew. We renovate your books, implement cutting-edge technology, and provide you with the real-time job costing and financial insights you need to make informed decisions. Our services are designed to give you peace of mind, allowing you to focus on what you do best - creating and building.

Here’s how we do it:

Schedule a conversation today, and in the meantime, download the Contractor’s Blueprint for Financial Success: A Step by-Step Guide to Maximizing Profits in Construction.” So you can stop worrying about accounting, technology, and compliance details and be free to hammer out success in the field.